When you hear "commercial crime insurance," don't let the name intimidate you. It’s simply a specialized policy built to protect your jewelry business from financial losses caused by crime. Think of it as a dedicated security system for your cash and accounts, guarding you against threats that your other policies, like property or general liability, just aren't designed to handle.

Why Jewelers Block Alone Is Not Enough

For any jeweler, a Jewelers Block insurance policy is the absolute cornerstone of your insurance strategy. It’s the essential coverage that protects your precious inventory—your rings, necklaces, and loose stones—from physical loss or damage, whether from a burglary, a fire, or even an accidental drop.

But what happens when the theft isn't a smash-and-grab? What if it's a silent, digital heist that drains your bank account, or a betrayal by a trusted employee?

This is exactly where commercial crime insurance proves its worth. While Jewelers Block acts as the vault protecting your physical assets, commercial crime coverage is the sophisticated surveillance system monitoring your financial transactions. It addresses the crimes that don't involve physically stealing jewelry, but instead target your cash, securities, and digital funds.

The Hidden Risks in a Jewelry Business

The high value and portability of your inventory obviously make you a prime target for thieves. But some of the most devastating financial hits come from sources you might not expect. A truly complete insurance plan has to account for these internal and digital threats.

These are the risks that almost always fall outside the scope of a standard Jewelers Block policy, creating dangerous gaps in your protection. This is precisely why a layered approach, combining both policies, is so crucial for any insurance for jewelry business.

A common misunderstanding is that a Jewelers Block policy covers every type of theft. While it’s brilliant at protecting your physical inventory, it often excludes losses from employee dishonesty, forgery, or computer fraud—the very risks that directly threaten your company's cash flow and long-term financial health.

Let's take a quick look at the primary threats this policy is designed to handle.

Crime Risks Every Jewelry Business Faces

| Type of Crime | Potential Perpetrator | Business Asset at Risk |

|---|---|---|

| Employee Theft | A trusted long-term employee, bookkeeper, or manager | Cash from the register, stolen checks, fraudulent invoices |

| Computer & Funds Transfer Fraud | An external hacker or an organized crime ring | Money in your business bank accounts, digital wallet funds |

| Forgery or Alteration | An employee, a sophisticated external fraudster | Company checks, withdrawal slips, financial documents |

| Robbery & Burglary (of Money) | An external criminal | Cash, money orders, or securities kept on-premises |

| Counterfeit Currency | A customer or professional counterfeiter | The cash value of fraudulent bills accepted during a sale |

As you can see, the dangers go far beyond a simple grab-and-run. These crimes attack the financial heart of your business.

Understanding the Complementary Roles

The easiest way to understand this is to think of your insurance like a two-part security system. Each part has a distinct, vital job to do.

-

Jewelers Block Insurance: This is your physical fortress. It protects tangible items like the stunning diamond rings in your display case, the loose stones in your vault, and the pieces you're shipping to a client. Its main purpose is to cover the loss of your actual stock-in-trade.

-

Commercial Crime Insurance: This is your financial cybersecurity and internal fraud detection team, all in one. It protects your liquid assets—the money in your bank accounts and digital payment systems. It's what steps in when an employee forges a check, a hacker tricks your bookkeeper into wiring funds to a fraudulent account, or you unknowingly accept a stack of counterfeit bills.

{kind=link}

Without commercial crime insurance, your business is left wide open to significant financial harm that could put its very survival at risk. Here at First Class Insurance, our Jewelers Block insurance specialists can help you see exactly how these coverages fit together. To find out just how affordable this essential protection can be, you can easily Get a Quote for Jewelers Block and crime coverage designed specifically for your operations.

Understanding Your Core Policy Protections

Let's be honest, trying to read an insurance policy can feel like wading through legal jargon. To really get what commercial crime insurance coverage does for you, we need to forget the dense policy language and think in terms of real-world situations. We’re going to break down the "insuring agreements"—the actual promises your insurer makes to protect your jewelry business.

Think of these agreements like different tools in a sophisticated security system. Each one is designed to handle a very specific type of financial threat. When you know what each tool does, you can see how the whole system works together to guard your assets.

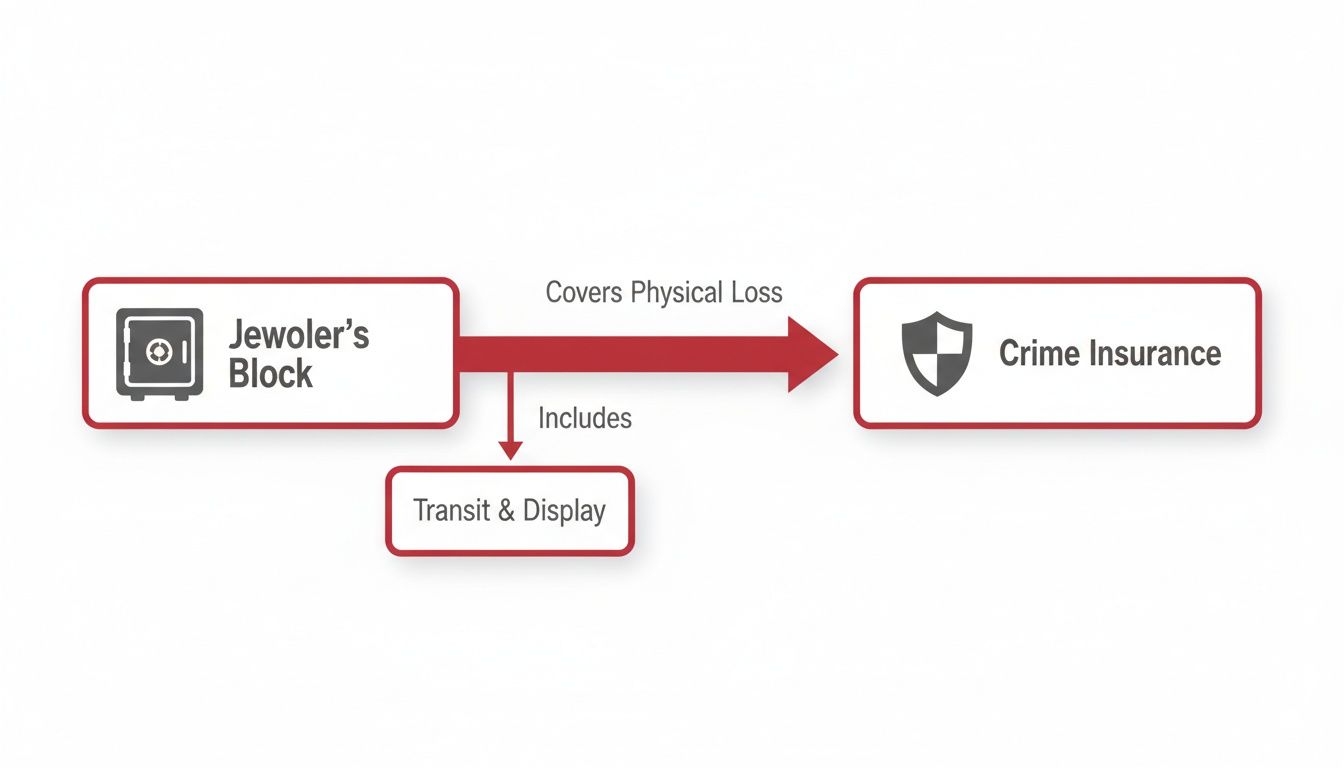

This diagram shows how crime insurance fits in, working alongside your main Jewelers Block insurance policy to cover the financial side of your business.

While your Jewelers Block is the bedrock for protecting physical inventory, crime insurance is the essential layer that protects your cash and financial accounts.

Employee Dishonesty and Theft

It's a tough pill to swallow, but some of the most devastating losses come from the inside. Employee Dishonesty coverage (also known as an employee theft or fidelity bond) is your defense against financial damage caused by your own team. Internal theft isn’t just a possibility; it's a major threat that accounts for a huge chunk of business losses every year.

We're not talking about a smash-and-grab here. This is about calculated, quiet betrayal that can fly under the radar for months, sometimes even years.

- Real-World Scenario: Imagine your store manager, a trusted employee of ten years, develops a secret gambling addiction. For over a year, they start pocketing loose diamonds from wholesale shipments before they're even entered into your inventory system. The total loss adds up to $80,000. Because an employee's dishonest act caused this, your commercial crime policy is what kicks in to cover it.

This coverage is absolutely vital because a standard Jewelers Block policy—which handles external theft of your inventory—almost always excludes losses caused by employee dishonesty. That gap makes crime coverage a non-negotiable part of your risk plan.

Forgery or Alteration

Next up is a classic form of white-collar crime that hasn’t gone away. The Forgery or Alteration agreement protects you from losses when someone forges or changes checks, drafts, or other financial documents.

You might think check fraud is a thing of the past in our digital world, but it’s still a surprisingly common and expensive problem. This coverage is there for you when your business's own financial paperwork is turned against you.

- Real-World Scenario: A bookkeeper creates a fake vendor in your system called "Gemstone Polishers Inc." They then generate phony invoices from this "vendor," forge a manager's signature on the checks, and cash them. Over a year, they steal $45,000 before an audit uncovers the scheme. This direct loss from a forged check would be covered.

Computer and Funds Transfer Fraud

Now we get to the most modern and fastest-growing threat out there. Computer and Funds Transfer Fraud coverage is your shield against cybercriminals who trick you or your staff into wiring money to their accounts. This is usually done through social engineering, where a hacker pretends to be someone you trust.

These scams are incredibly effective because they prey on human error, not just software bugs. The FBI's Internet Crime Complaint Center (IC3) reports that business email compromise (BEC) schemes cost companies billions every single year.

- Real-World Scenario: Your accounts payable clerk gets an email that looks exactly like it's from your main diamond supplier. The email urgently requests that a $120,000 payment be sent to a "new" bank account for an "audit." Believing it's legitimate, your clerk wires the money. Just like that, you've sent a massive payment straight to a criminal. This is the exact kind of disaster that Funds Transfer Fraud coverage is built to stop.

Protecting Assets Beyond Your Storefront

Let's be honest—your vault and showroom aren't the only places your high-value inventory is at risk. For most jewelers, the most dangerous moments happen when your assets are on the move. That’s where you’re exposed, far from the safety of your alarms and safes.

This is exactly why off-premises protection is so critical.

A standard commercial crime policy is great for things like fraud or employee theft, but it's not built to cover physical inventory once it leaves your store. A proper Jewelers Block policy, on the other hand, is designed specifically to fill that gap. It protects your goods whether they're in transit or at any other location.

Without it, a single incident outside your store could become a catastrophic, uninsured loss.

High-Stakes Scenarios Outside Your Walls

The risks that come with off-premises inventory are both unique and severe. A simple theft or a moment of distraction can turn into a financial nightmare in a heartbeat. The right insurance for a jewelry store has to account for these real-world possibilities.

Just think about these all-too-common situations:

- Salesperson Robbery: A traveling sales rep is heading to a private viewing with a case full of diamond rings. They're targeted at a gas station or hotel, and just like that, you're facing a $250,000 loss.

- Shipping Disappearance: You ship a parcel of loose gems to a cutter using a secure courier. The package gets signed for at the facility but vanishes before it ever reaches its destination.

- Trade Show Theft: During the chaos of setting up at a big trade show, a display case of high-end watches is lifted from your booth while your team is distracted for just a moment.

In every one of these scenarios, the loss happened miles away from your store. A standard property or crime policy would almost certainly deny the claim, which is precisely why jewelers need specialized coverage that travels with their inventory.

The whole point of off-premises coverage is to extend the security of your vault to your inventory, no matter where it goes. It’s built on the reality that a huge part of your business happens on the road, in clients' homes, and at industry events.

How In-Transit and Off-Premises Coverage Works

This protection isn't just a simple add-on; it comes with its own set of rules and requirements designed to manage the extreme risk involved. Understanding these conditions is the key to making sure your coverage actually works when you need it most.

Your policy will have specific rules you have to follow to the letter. If you don't, you could put your entire claim in jeopardy.

Key Policy Requirements and Restrictions:

- Security Mandates: For high-value shipments, your policy might demand you use a specific armored transport service. If a salesperson is traveling with merchandise, it could require that the inventory is always attended or locked in a hotel safe.

- Geographical Limits: Coverage is often restricted to certain areas. For example, a policy might cover transit within the continental U.S. but exclude international shipments unless you add a specific endorsement.

- Specific Sublimits: The coverage amount for your off-premises inventory is usually a "sublimit"—a smaller amount than your total inventory coverage. Your policy might cover $2 million of inventory inside your store but have a $500,000 sublimit for any goods on the move.

It’s crucial to walk through these scenarios with an insurance professional who gets your business. At First Class Insurance Jewelers Block Agency, our experts can help you build a policy that truly protects your assets, from heirloom pieces to modern designs. You can see how we approach insuring specific high-value items in our guide to protecting antique jewelry collections. By carefully reviewing your day-to-day operations, we make sure your coverage matches your real-world risks—both inside your store and out.

{kind=link}

Navigating Common Policy Exclusions and Gaps

No insurance policy is a silver bullet. Knowing what your commercial crime insurance coverage doesn't protect is just as critical as knowing what it does. Think of your policy as a contract with very specific rules—it comes with exclusions that intentionally leave certain situations out. For a jeweler, some of these can feel like major vulnerabilities if you don't address them head-on.

These exclusions aren't there to trick you; they exist to define the policy's job and keep it from overlapping with other types of insurance, like your Jewelers Block insurance policy. They often pop up in situations where the proof of a crime is fuzzy or the loss comes from a different kind of business risk altogether.

What Your Policy Typically Will Not Cover

It's absolutely essential to get familiar with these common exclusions because they represent the built-in gaps in your protection. Without adding a special fix to your policy, you could be left holding the bag for a massive financial loss.

Here are some of the most frequent exclusions you'll find in a standard policy for an insurance for jewelry business:

- Acts by Partners or Owners: This is a big one. Standard employee dishonesty coverage is for just that—employees. It specifically carves out fraudulent acts committed by the business owners, partners, or members of an LLC.

- Voluntary Parting: If you're tricked into willingly handing over jewelry, the policy won't step in. A classic example is a scammer who convinces you to ship a piece on the promise of a wire transfer that never shows up.

- Inventory Shortages: Let's say a routine inventory count shows you're missing several diamonds. If you have no proof of how they disappeared—no security footage, no forced entry, no confession—the policy won't cover it. Insurers often call this a "bookkeeping" loss.

- Cyber-Related Losses: While a crime policy covers certain types of fraud, it's not a cybersecurity policy. Losses from a data breach, a ransomware attack, or other direct cyber events are almost always excluded and fall under a separate Cyber Liability policy.

The common thread here is the need for direct proof of a criminal act. Your insurer needs to see clear, undeniable evidence that a covered crime—like theft or forgery—was the direct cause of your financial loss.

Closing the Gaps with Policy Endorsements

This is where having a serious conversation with your insurance agent pays off. You can often plug these holes by adding endorsements, sometimes called riders, to your policy. An endorsement is a special modification that adds or changes your coverage, letting you build protection that fits the unique world you operate in.

One of the most valuable endorsements a jeweler can get is for Mysterious Disappearance.

This rider is designed specifically to close the gap left by that inventory shortage exclusion. With this protection added, if an item vanishes from a locked case or your vault with no explanation and no sign of a break-in, the coverage can step in. It takes the pressure off you to prove exactly what crime occurred.

Other endorsements can be added to cover losses from specific social engineering scams or to expand protection to cover people who might not fit the classic definition of an employee. By working with a specialist at an agency like First Class Insurance Jewelers Block Agency, you can pinpoint these weak spots and build a policy that truly protects your assets. When you Get a Quote for Jewelers Block and crime coverage, make sure you ask about these critical add-ons.

How Your Policy Limits, Deductibles, and Premiums Work

To really get a grip on your commercial crime insurance coverage, you have to understand its financial architecture. This isn't just fine print; it's the blueprint that dictates how much protection you actually have, what you’ll pay out-of-pocket, and how your premiums are calculated.

The three pieces you need to master are your limits, deductible, and premium. Nailing these down means you get the right level of protection for your jewelry business without overpaying for coverage you don't need.

Decoding Your Policy Limits and Sublimits

Your overall policy limit is the easiest number to find. It’s the maximum amount an insurer will pay out for a covered loss during your policy period. For example, your policy might have a $1 million limit. Simple enough.

But the devil is in the details, and in insurance, the details are the sublimits. A sublimit is a smaller cap buried within your main policy that applies to a specific type of crime. Insurers use these to manage their risk for high-frequency events, like digital fraud, which is a huge exposure for any business today.

Here’s a real-world example for an insurance for a jewelry store:

- Main Policy Limit: $1,000,000

- Computer Fraud Sublimit: $100,000

- Forgery Sublimit: $100,000

In this scenario, while you technically have a million dollars of protection, your insurer will only pay up to $100,000 if you get hit with a wire transfer scam. Knowing these sublimits is absolutely critical—ignoring them is how you end up dangerously underinsured for the most likely threats.

Understanding Your Deductible

The deductible is your skin in the game. It’s the amount of money you have to pay out of your own pocket before your insurance coverage kicks in.

Think of a deductible as your financial stake in the claim. A higher deductible typically means a lower premium, but it also means you absorb more of the cost if a crime occurs. Conversely, a lower deductible gives you more first-dollar protection but results in a higher premium.

Let’s say your jewelry store insurance covers a $50,000 loss from employee theft. If your policy has a $5,000 deductible, you pay the first $5,000. Your insurance company then picks up the remaining $45,000, right up to your policy limit.

Key Factors That Determine Your Premium

What you actually pay for coverage—the premium—isn't just a number pulled from a hat. Underwriters, like those from our partners which you can learn more about in this guide to Lloyd's of London, dig into a whole range of factors to figure out your unique risk profile.

{kind=link}

And the demand for this protection is only growing. The fidelity and crime insurance market is expected to jump from US$ 724 million in 2025 to US$ 1,114 million by 2031. This surge is fueled by rising crime, especially internal fraud—employee dishonesty claims alone account for roughly 40% of all fidelity payouts worldwide. You can dive deeper into these trends in this detailed market research.

So, what are underwriters looking at?

- Annual Revenue and Asset Value: Bigger businesses with more valuable assets simply have more at stake, increasing their risk exposure.

- Number of Employees: More people on payroll can, statistically, increase the chances of internal theft.

- Internal Security Controls: This is a big one. Strong protocols, like requiring dual signatures on checks or conducting regular audits, can seriously lower your premium.

- Claims History: A track record of frequent claims signals a higher future risk, and your pricing will reflect that.

Filing a Claim and Strengthening Your Defenses

That gut-wrenching moment you discover your business has been hit by crime is something no owner wants to experience. In the middle of that chaos, your commercial crime insurance coverage is supposed to be your lifeline. But knowing exactly what to do—and when—is what separates a smooth recovery from a nightmare.

Before you do anything else, call the police. A formal police report isn't just a formality; it's the foundational document for your entire insurance claim.

Once that’s done, your very next call should be to your insurance agent. Get the ball rolling immediately. They’ll tell you exactly what paperwork and proof-of-loss forms you’ll need to fill out.

From there, your job is to become an evidence librarian. Secure every shred of proof you can find—security footage, dodgy emails, altered invoices, you name it. Don't delete or throw away a single thing. These items are gold for the police investigation and absolutely critical for your insurer’s review.

Your Step-by-Step Claim Filing Process

Trying to navigate a claim during a crisis can feel overwhelming. The key is to break it down into a simple, logical sequence.

- Immediate Notification: The second you discover the crime, get law enforcement and your insurance broker on the phone. Time is critical.

- Evidence Preservation: Lock down and make copies of all video, documents, and digital trails connected to the incident.

- Detailed Documentation: Write down everything you know: the date, the exact amount lost, who was involved, and a clear story of how the crime went down.

- Formal Claim Submission: Your insurer will send you an official "proof of loss" form. Fill it out completely and attach all the evidence you’ve collected.

- Cooperation with Adjuster: The insurance adjuster is your main point of contact. Be responsive and provide any extra information they need right away. This keeps your claim moving forward.

Proactive Prevention: Your First Line of Defense

While insurance is essential for recovery, the smartest move is always to stop crime before it even starts. Think of strong internal controls as your most powerful security system. They don’t just reduce your risk; they show underwriters you’re a well-run business, which can help keep your premiums in check.

The global crime insurance market was valued at $16.25 billion in 2024 and is projected to hit $63.56 billion by 2035, a clear sign that businesses everywhere are waking up to the growing threat.

Your internal security protocols are more than just a rulebook; they’re an active deterrent. The harder you make it for criminals to succeed, the less likely they are to target you in the first place.

While commercial crime insurance offers a financial backstop, pairing it with physical security upgrades from professional commercial locksmith services creates a much tougher defense. For an insurance for a jewelry business, this combination of physical security and strict internal procedures is the gold standard for risk management.

Here's a practical checklist you can use to tighten your defenses today:

- Conduct Thorough Background Checks: Never grant an employee access to high-value inventory or sensitive financials without verifying their history first.

- Enforce Strict Inventory Controls: Set up a system for regular, independent audits and cycle counts. This is the fastest way to spot if something is missing.

- Require Dual Authorization: For any large financial transaction—like a wire transfer or check payment above a set amount—make it a rule that two authorized people must sign off. No exceptions.

- Provide Ongoing Security Training: Your staff is on the front lines. Train them regularly to spot phishing attempts, social engineering scams, and other common ways fraudsters try to get in.

Your Top Insurance Questions, Answered

Let's cut through the noise. When it comes to commercial crime and Jewelers Block insurance, you probably have a lot of questions. Getting straight answers is the only way to make the right call for your business. Here’s a breakdown of what jewelers ask us most.

What’s the Real Difference Between Jewelers Block and Commercial Crime Insurance?

Think of it like this: your Jewelers Block policy is the vault, protecting your physical goods. Its main job is to cover your tangible inventory—the diamonds, watches, and finished pieces—from physical threats like a smash-and-grab robbery or a fire.

Commercial crime insurance, on the other hand, guards your cash flow. It’s built to protect your liquid assets—the money in your bank accounts and your register—from financial crimes like an employee embezzling funds, someone forging a check, or a hacker tricking you into a fraudulent wire transfer. You absolutely need both.

Is My Jewelry Store Insurance Expensive?

There’s no one-size-fits-all answer. The cost of jewelry store insurance really comes down to your specific risk profile. Underwriters look at a handful of key factors to figure out what your premium should be.

Here's what they're looking at:

- Inventory Value: How much jewelry do you have on hand?

- Annual Revenue: Higher sales can mean more exposure to different kinds of risk.

- Security Measures: Your vault, safes, and alarm systems matter. A lot.

- Internal Controls: Things like background checks and requiring two people to sign off on large payments can significantly lower your risk—and your premium.

- Location and Claims History: Where your store is located and your past loss history are big parts of the equation.

Why Won’t My Jewelers Block Policy Cover Employee Theft?

This is a critical distinction that trips up a lot of jewelers. Your Jewelers Block insurance policy is designed to cover losses from outside threats, like a burglary or a mysterious disappearance of a tray of rings. These policies almost always have a crystal-clear exclusion for dishonest acts committed by your own team.

Insurers see internal theft as a completely different kind of risk. It’s not about an external criminal breaking in; it’s about a breach of trust from within. That’s exactly why you need a separate commercial crime policy with its specific Employee Dishonesty coverage.

Without it, you’re leaving your business wide open to one of the most common and financially devastating threats in our industry.

At First Class Insurance, we don't just sell policies; we build protection that covers every angle of your business. Our experts at the First Class Insurance Jewelers Block Agency will put together a plan that combines the robust inventory protection you need with the essential commercial crime coverage you can't afford to be without.

See how we can secure your assets and give you peace of mind.