When a customer hands you their family heirloom for repair or a high-value piece for consignment, their trust is in your hands. They need to know, without a doubt, that you’ve got their back. That's where the terms bonded and insured come into play. People often use them interchangeably, but they are two completely different layers of protection.

Here's the bottom line: insurance protects your jewelry business from disasters like a smash-and-grab robbery or a fire. A surety bond protects your customers if you fail to deliver on a promise or if an employee acts dishonestly.

Understanding the Key Differences

For a jeweler, getting this right isn't just about semantics—it’s about solid risk management and building a reputation that attracts high-value clients. Think of it this way: insurance is the shield that defends your assets. A bond is a public promise, a guarantee of your professional integrity.

This distinction becomes critical when you're handling a customer's property for an off-site appraisal, taking in a million-dollar piece on consignment, or doing a complex custom design. In these moments, your client’s peace of mind is just as valuable as the gemstone on your bench.

Bonded vs Insured At a Glance for Jewelers

To make it crystal clear, let's put these two protections side-by-side. This table breaks down what each one really does for a jewelry business like yours.

| Aspect | Bonded (Surety Bond) | Insured (e.g., Jewelers Block insurance) |

|---|---|---|

| Who is Protected? | Primarily the customer (the "obligee"). | Primarily the jewelry business (the "insured"). |

| What is Covered? | Failure to meet contractual obligations, fraud, or employee theft affecting a client. | Direct physical loss or damage to your inventory, premises, and customer property in your care. |

| Primary Purpose | To guarantee your business's performance and ethical conduct. | To transfer your business's financial risk of loss to an insurance company. |

Seeing them laid out like this makes the different roles obvious. One is a customer-facing guarantee, while the other is an internal safety net for your business.

The Nature of the Agreement

The mechanics behind these protections are fundamentally different. Insurance is a simple, two-party contract between you and your insurer. A covered loss happens, you file a claim, and the insurance company pays you according to your policy. It's a direct relationship.

A surety bond, on the other hand, is a three-way handshake between:

- The Principal: Your jewelry business, making the promise.

- The Obligee: Your customer, who is receiving the promise.

- The Surety: The company financially guaranteeing your promise.

If you break that promise and a valid claim is filed, the surety company pays your customer to make them whole. But it doesn't end there. The surety then comes to you for full reimbursement. It’s less like insurance and more like a line of credit that backs your word.

Market Significance and Application

This model of guaranteeing performance isn't niche; it's a cornerstone of commercial trust that you see in all kinds of industries. The global surety bond market is on track to hit $27 billion by 2030, which shows just how much businesses rely on this to operate. You can learn more about the growth of the bond insurance market and its role in commerce.

For your jewelry store, being bonded isn’t just a formality. It’s a powerful marketing tool that tells customers you stand behind your work with a financial guarantee—a level of assurance that insurance alone just can't provide.

How Surety Bonds Build Client Trust

When you tell a client you're bonded, you're doing more than just sharing a business credential. You're making a public promise about your integrity, backed by a powerful financial guarantee. It’s a message that says your jewelry business stands behind its obligations, offering a level of security that insurance alone can't touch. In the high-stakes world of jewelry, understanding the difference between bonded vs. insured can be the very thing that earns a client's peace of mind.

A surety bond isn't like a straightforward, two-party insurance policy. It's a three-party agreement, and knowing who's who is crucial to seeing its value.

- The Principal: That's your jewelry business. You're the one promising to perform a service ethically and follow through on your contracts.

- The Surety: This is the bonding company, the financial guarantor that backs your promise with its own capital.

- The Obligee: This is your client. They are the ones protected by the bond and can make a claim if you fail to deliver.

Think about it this way: before a surety company issues you a bond, they dig into your business's financial health and reputation. Their willingness to back you is a powerful third-party endorsement of your trustworthiness before you even speak to a client.

How Bonds Protect Your Jewelry Clients

Bonds aren't a one-size-fits-all solution. They are tailored to tackle specific risks and build credibility where it matters most. For jewelers, a couple of bond types are especially powerful for building client confidence.

A business service bond is a great example. Say you send an appraiser to a client's home to value a private collection. If an employee were to steal something, this bond protects your client from the financial loss. It directly answers the "what if" question about employee dishonesty, which is a major concern for anyone letting you into their home. Offering this protection sends a clear signal of professionalism.

Another critical one is a consignment bond. When an artist or another dealer trusts you to sell their work, they need to know they'll either get paid or get their piece back safely. A consignment bond guarantees it. It protects the artist (the obligee) if your business fails to hold up its end of the deal, making it an essential tool for sourcing unique, high-value inventory.

It's a common mistake to think a surety bond is insurance for your business. It’s not. It acts more like a line of credit that protects your client. If the surety pays a claim, you are contractually required to pay them back in full.

The Financial Reality of a Bond Claim

That repayment clause is the absolute core difference between being bonded and insured. An insurance company absorbs the financial loss from a covered claim. A surety company does not. The bond exists to make your client whole first, ensuring they aren't left with a financial hole because of something your business did.

Once the surety pays that claim, they will come to you, the principal, to recover every dollar. This structure holds your business accountable for its promises. And frankly, that commitment to accountability is precisely why being bonded is such a powerful signal of reliability in the market.

For many in our industry, this layer of protection is amplified by professional memberships. Being part of a group like the Southern Jewelry Travelers Association (SJTA), for example, already shows a commitment to high standards. A bond just solidifies that reputation, proving you're willing to back it up with a financial guarantee.

{kind=link}

Protecting Your Assets with Jewelers Block Insurance

While a surety bond protects your clients from you, insurance is the shield that protects your business from the world. It's a completely different animal. In the high-stakes world of jewelry, insurance isn't just a good idea—it's the financial bedrock your business stands on.

The core distinction in the bonded vs. insured debate is this: insurance is a two-party agreement between you and an insurer. Its sole purpose is to take the risk of catastrophic loss off your shoulders and transfer it to theirs.

For a jeweler, any old business insurance policy is a recipe for disaster. You need coverage built for the unique dangers you face daily, from smash-and-grabs to sophisticated heists. This is exactly why Jewelers Block insurance was created. It's a comprehensive safety net designed specifically for your high-value inventory, closing the dangerous gaps a standard policy leaves wide open.

What Does Jewelers Block Insurance Cover?

A bond only pays out if you fail to meet an obligation. A Jewelers Block insurance policy, on the other hand, responds to direct physical loss or damage to your inventory—the lifeblood of your entire operation. It's designed to protect your assets whether they're locked in a vault, sitting in a showcase, or on their way to a client.

Here are a few of the unique risks a specialized Jewelers Block policy is built to handle:

- Theft: This covers the full spectrum, from a brazen daylight robbery to a quiet, sophisticated overnight burglary.

- Fire and Water Damage: It provides coverage if a fire, flood, or even a burst pipe from the apartment upstairs ruins your inventory.

- Damage in Transit: It protects your pieces while being shipped to a customer or transported between locations—a time when they are incredibly vulnerable.

- Customer Property: This is critical. It covers customers' jewelry left with you for repair, appraisal, or consignment. This protects not just your finances, but your hard-earned reputation.

Let's clear up a common, and costly, misconception: a General Liability policy does not cover your inventory. That policy is for things like a customer slipping and falling in your store. It does nothing for your stolen or damaged jewelry. Only Jewelers Block insurance protects your actual product.

Insurance in Action: A Practical Example

Picture this: a water pipe bursts in the ceiling above your shop overnight. You arrive in the morning to find your showroom flooded, ruining several high-end watches and a handful of custom pieces customers had left for repair.

A surety bond is useless here—you didn't break any promises. Your General Liability policy might help with the soggy drywall and warped flooring, but it won't touch the priceless inventory sitting in ruined display cases.

This is where your Jewelers Block insurance saves your business. You file a claim directly with your insurer, and the policy kicks in to cover the cost of repairing or replacing not just your damaged stock, but your customers' property as well. This is the direct financial lifeline that lets you recover from a disaster and get back to business. It's the only way to truly guarantee the protection of a diamond ring and all the other valuables under your roof.

{kind=link}

The Broader Insurance Landscape

The global insurance industry, which collected a staggering €7.0 trillion in premiums in 2024, is built on a clear separation between insurance products and surety bonds. That distinction is especially vital in the U.S. market, where the surety industry wrote $9.3 billion in premiums in 2023. At the end of the day, insurance for your jewelry business is about asset protection. Bonds are about performance guarantees.

A robust insurance plan, anchored by a policy from an expert First Class Insurance Jewelers Block Agency, is your first and best line of defense against the unexpected. When you pair it with a solid general liability policy, you build a financial shield that allows your business to not just survive a disaster, but to thrive in spite of it.

Comparing Coverage in Real-World Scenarios

Knowing the dictionary definition of "bonded" versus "insured" is one thing. Seeing how they perform in a crisis is another entirely. Let's get out of the textbook and walk through a few real-world situations jewelers actually face, so you can see where each one steps up and where it steps aside.

The real question to ask is: who needs protection, and from what? Is it your business needing a financial backstop after a catastrophe? Or is it your client needing a guarantee that you'll operate with integrity? The answer tells you which tool you need.

H3: Scenario 1: Employee Theft During a Private Viewing

Imagine this: you send a trusted senior employee to a client's home for a private viewing and appraisal. A week later, you get a panicked call. The client claims a $50,000 vintage diamond bracelet is missing from a jewelry box in the room where your employee was working.

-

A Surety Bond's Role: This is exactly what a business service bond is for. Your client (the obligee) files a claim against the bond. The surety investigates, finds the claim valid, and pays the $50,000 directly to your client, making them whole. But it doesn't stop there. The surety then comes to you, the business owner (the principal), to be reimbursed for the full amount they paid out.

-

Jewelers Block Insurance's Role: Your Jewelers Block insurance policy probably wouldn't touch this. This kind of insurance is designed to protect your inventory and customer property while it's in your care, custody, and control. Since the theft happened at the client's home and involved their property, it falls outside the policy's protective bubble.

The takeaway here is clear: a bond protects your client from dishonest acts your employees might commit on their property.

H3: Scenario 2: A Devastating Overnight Fire

Now for a different kind of disaster. A fire rips through your building overnight. Despite the fire department's best efforts, your store is gone. Your entire inventory, plus all the consignment pieces and customer repairs, is destroyed.

-

A Surety Bond's Role: A bond is useless here. You didn't commit fraud or fail to meet a contractual obligation—you were the victim of a random catastrophe. Bonds simply aren't designed to cover property damage from external events like a fire.

-

Jewelers Block Insurance's Role: This is where Jewelers Block insurance becomes your lifeline. As a two-party contract between you and your insurer, its entire purpose is to protect your business assets. You file a claim, and your insurer pays to replace your inventory and cover the value of the customer property you were holding. It’s what allows a business to survive a catastrophic loss.

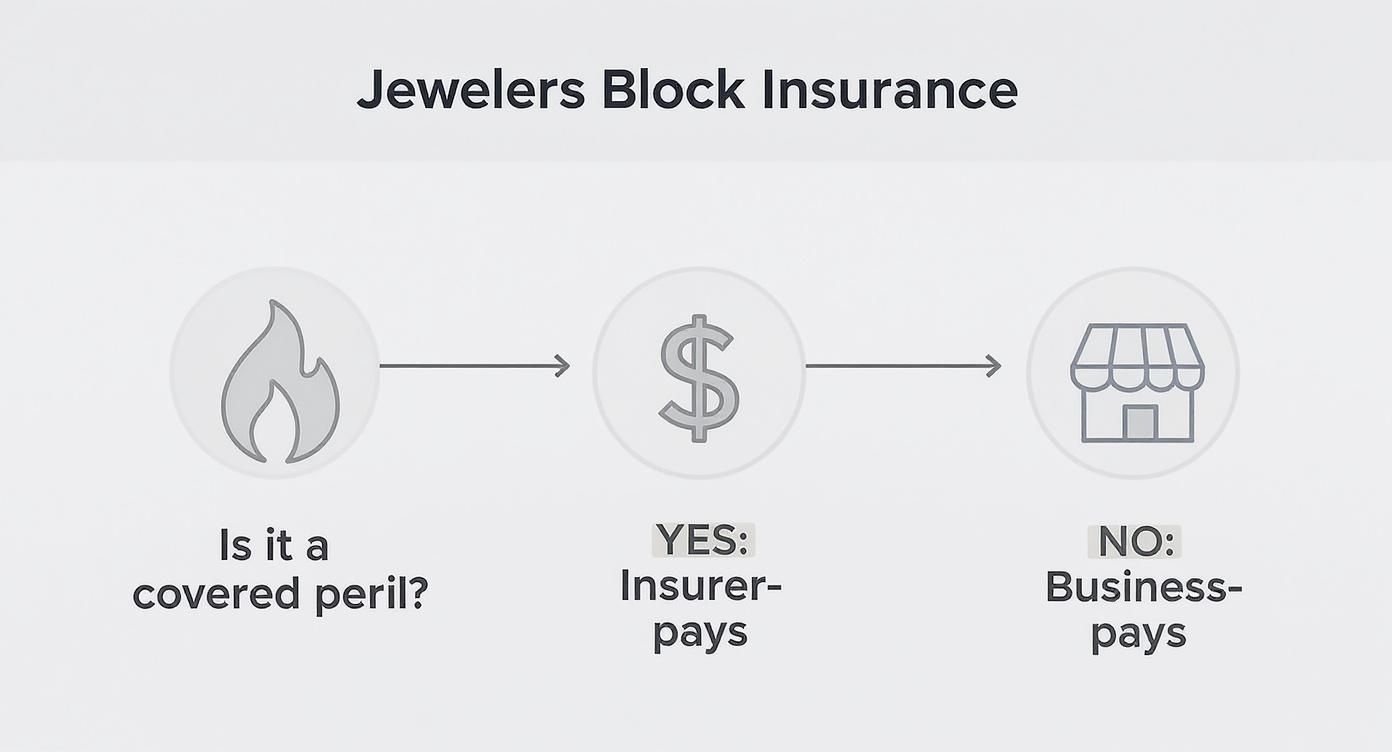

This flowchart breaks down exactly how a Jewelers Block policy kicks in when a covered event, like a fire, happens.

As you can see, if the incident is a covered peril, the insurer pays the loss. This is what keeps your business from financial ruin.

H3: Scenario 3: Failure to Return Consignment Jewelry

Let's try one more. A designer consigns a valuable collection with your store. But your business hits hard times, closes its doors suddenly, and you can't pay the designer for the items you sold or return the unsold inventory.

-

A Surety Bond's Role: The designer can file a claim against your consignment bond. The surety company pays the designer for the value of their lost or unreturned jewelry, up to the bond's limit. And just like before, the surety will then come to you for full reimbursement. The bond is a financial guarantee that you'll uphold your end of the consignment deal.

-

Jewelers Block Insurance's Role: Your insurance policy won't respond here. This isn't a case of physical loss or damage; it's a breach of contract stemming from financial failure. Insurance isn't there to cover losses from poor business management.

The need for this kind of guaranteed performance is growing. In the first half of 2021, for instance, the volume of insured municipal bonds in the U.S. hit $10.74 billion, a huge jump from $7.84 billion in 2020. You can see more on the growing preference for bond insurance and why this trend matters.

These scenarios make the distinction between bonds and insurance incredibly clear. To put it all in one place, here’s a quick-glance table comparing how each would respond to common incidents.

Bond vs Insurance Response to Common Jewelry Business Incidents

| Incident Scenario | Surety Bond Response | Jewelers Block Insurance Response | Key Takeaway |

|---|---|---|---|

| Employee Steals from Client's Home | Responds. The business service bond pays the client for the theft, then requires the jeweler to reimburse the full amount. | Does Not Respond. The loss occurred outside the jeweler's premises and did not involve the jeweler's own inventory. | A bond protects your clients from your employees' dishonest acts. |

| Overnight Fire Destroys Store | Does Not Respond. This is an external catastrophe, not a failure of the jeweler to perform a duty. | Responds. The policy covers the loss of the jeweler's inventory and customer property in their care, custody, and control. | Insurance protects your business assets from physical loss or damage. |

| Failure to Pay Consignor | Responds. The consignment bond pays the designer for the unreturned inventory, then seeks reimbursement from the jeweler. | Does Not Respond. This is a breach of contract and financial failure, not a covered physical peril. | A bond guarantees your contractual obligations to partners. |

| Customer Slips and Falls in Store | Does Not Respond. This is a liability issue, not a contractual or fidelity failure. | Does Not Respond (Typically). General liability coverage, often separate or bundled with a BOP, would handle this. | Neither a bond nor a standard Jewelers Block policy covers general liability claims. |

At the end of the day, both bonds and insurance are about building trust and security. One shows clients and partners you're reliable, while the other ensures your business can survive the unexpected.

A bond is your promise backed by money. Insurance is your shield against disaster. One covers your integrity; the other covers your assets. Understanding this difference is the key to building a truly protected jewelry business.

Understanding the Financial Differences

Beyond the fundamental question of who they protect, bonds and insurance are two completely different animals when it comes to their financial mechanics. For any jeweler, getting a handle on these differences—from how premiums are set to how claims are paid—is critical for managing your risk and your cash flow. This isn't just about coverage; it's about your bottom line.

Think of it this way: a bond's cost is a reflection of your trustworthiness. An insurance premium, on the other hand, is a reflection of the outside world's threats to your business.

How Costs Are Calculated

Calculating a surety bond premium is a very personal affair. The cost is usually a small slice of the total bond amount, typically somewhere between 1% and 5%. What drives that rate up or down? Your personal credit score and the financial health of your jewelry business. If you have a rock-solid financial history, the surety company sees you as a low-risk principal and rewards you with a lower premium.

Jewelers Block insurance premiums are a different story altogether. The calculation is based on a much wider set of variables tied directly to physical risk. An underwriter from a top-tier provider, like those at Lloyd's of London, will dig into the specific details of your operation.

![]()

They'll assess factors like:

- Inventory Value: The total dollar amount of the jewelry, diamonds, and precious metals you have on hand.

- Vault Specifications: The grade and security features of your safes and vaults.

- Security Systems: The quality of your alarm systems, surveillance cameras, and access controls.

- Geographic Location: The specific crime rates and risks tied to your store’s neighborhood.

This deep dive results in a premium that truly reflects the real-world dangers your assets face every single day.

The Critical Difference in the Claims Process

Here’s where the rubber really meets the road. The single most important financial distinction between being bonded and insured shows up when a claim is filed. Every jeweler needs to burn this concept into their memory because it has a direct impact on both your business and personal finances.

With an insurance claim, the process is pretty straightforward. A covered disaster strikes—a smash-and-grab theft, a fire, a burst pipe—and you file a claim with your insurer. After they investigate and approve it, the insurance company cuts you a check to cover the loss, absorbing the financial hit as laid out in your policy. The money flows from the insurer to you.

A bond claim operates in the complete opposite direction. The surety company pays your client first to make them whole, but that payment is effectively a loan made to you. You are now legally on the hook to reimburse the surety company for every single penny they paid out, plus any administrative fees.

This repayment obligation is the absolute core of the financial difference. With insurance, you transfer your risk to the insurance company. With a bond, you are ultimately still responsible for the financial loss; the bond just acts as a guarantee that your client gets paid right away.

For those interested in how technology is changing financial oversight, learning about AI-powered financial analysis can provide valuable insights. Understanding these mechanics helps you manage your liabilities effectively. At the end of the day, a bond guarantees your word with a financial backstop you must repay, while insurance protects your assets from a catastrophe you can't control.

Building a Complete Risk Management Strategy

It's a huge mistake to see the "bonded vs. insured" debate as an either/or decision. They aren't in competition. Smart jewelers know these are two different tools for two totally different jobs. Your insurance is the internal shield protecting you from a catastrophic loss. A bond is your external promise—a guarantee of your integrity to clients and partners.

The goal isn't to pick one; it's to build a complete risk management portfolio that protects both your balance sheet and your reputation.

The first step is a gut check on how your business actually runs. A few straightforward questions will cut through the noise and tell you if a bond is a must-have addition to your core Jewelers Block insurance. This isn't theoretical. It’s about matching your protection to what you do every single day.

A Practical Checklist for Your Jewelry Business

Ask yourself these questions. The answers will tell you if your risk profile demands both.

- Do my employees handle client property off-site? If you’re doing in-home appraisals or private showings, a business service bond is non-negotiable. It protects your clients from the worst-case scenario of employee theft.

- Do I manage high-value consignment items? For any jeweler working with designers or other dealers, a consignment bond is an essential tool. It’s how you build trust and secure those crucial inventory partnerships.

- Are bonds required for any municipal licenses or contracts? Sometimes, the choice isn't yours. Local regulations or even a commercial lease might legally require your store to be bonded to operate.

If you answered "yes" to any of these, a surety bond is almost certainly a vital piece of your strategy. Of course, beyond financial products, simply understanding solid general contract signing practices is another crucial element in building a complete risk management strategy.

Finding the Right Protection Partner

Once you know what you need, the next step is getting it from the right people. When it comes to insurance for a jewelry store, you absolutely must work with a specialist. A first-class First Class Insurance Jewelers Block Agency brings deep industry knowledge that a general insurance agent just can't replicate. They get the nuances of vault ratings, secure transit protocols, and how to properly value your inventory.

When you decide to get a quote for Jewelers Block, look for an agency that acts more like a partner than a provider. They should be asking you the tough, detailed questions about your operations. That's how you know they're focused on plugging every potential gap in your insurance for jewelry business needs.

At the end of the day, you're building a tailored protection plan. An expert agency can help you weave the right jewelry store insurance together with any necessary bonds. The result is a formidable defense that secures your financial future and reinforces the trust you've worked so hard to build.

Frequently Asked Questions

Let's cut through the noise. Here are some of the most common questions we hear from jewelers trying to sort out the whole bonded vs. insured debate.

I Already Have Jewelers Block Insurance. Do I Really Need to Be Bonded, Too?

More than likely, yes. It's a classic case of apples and oranges—they both offer protection, but for completely different things. Your Jewelers Block insurance is the bedrock policy that protects your property from physical losses like theft or fire.

A surety bond, on the other hand, protects your clients. It’s a guarantee to them that you’ll operate ethically and fulfill your promises. If you do appraisals in clients’ homes or handle high-value consignments, that bond is what gives them the confidence to hand over their precious items. It’s a non-negotiable layer of trust.

How Much Does It Cost to Get a Jewelry Business Bonded?

The cost of a bond, called the premium, is a fraction of the total bond amount you need. Typically, you're looking at anywhere from 1% to 5% of the bond value per year.

What pushes you to one end of that range or the other? It comes down to risk. The surety company will look at your personal credit score and your business's financial stability. A solid financial track record means less risk for them, which translates directly into a lower premium for you.

Can a Customer Actually Verify if My Store Is Insured and Bonded?

They absolutely can, and you should encourage it. Transparency is your best friend here. For the bond, a customer can simply ask for your bond number and contact the surety company that issued it to confirm it’s active.

For your insurance, you can provide a Certificate of Insurance (COI). This is a standard document from your First Class Insurance Jewelers Block Agency that proves you have active insurance for a jewelry store. Being upfront with this information doesn't just answer a question—it builds instant trust.

Where Can I Get a Quote for Jewelers Block Insurance?

Steer clear of general insurance agents. You need to work with a specialist who lives and breathes the jewelry industry every single day. Someone who provides jewelry store insurance understands the nuances of inventory risk, secure transport, and all the specific dangers your insurance for jewelry business needs to cover.

An industry expert can look at your specific operation—from your safe ratings to your travel schedule—and structure a policy that actually protects you, no gaps attached.

At First Class Insurance, we do one thing: build risk management solutions for jewelers. Your life's work is too valuable to leave vulnerable. Get a Quote for Jewelers Block and get the peace of mind you deserve.