How Much Is Jewelry Insurance? A Guide to Protecting Your Valuables

So, you're wondering what jewelry insurance actually costs? The good news is, there's a pretty reliable rule of thumb. Generally, you can expect to pay somewhere between 0.5% and 2.5% of your jewelry's total appraised value each year for coverage.

But that range is just a starting point. The real question is whether you're protecting a personal treasure or an entire business inventory, because that’s where the numbers really start to diverge.

Answering The Core Question: How Much Is Jewelry Insurance?

The world of jewelry insurance is split into two very different paths: personal policies and commercial policies. They cover different things, are priced differently, and are built to handle completely separate levels of risk.

A personal policy is designed for things like your engagement ring, a family heirloom, or that luxury watch you wear every day. It’s focused on protecting individual pieces from loss, damage, or theft.

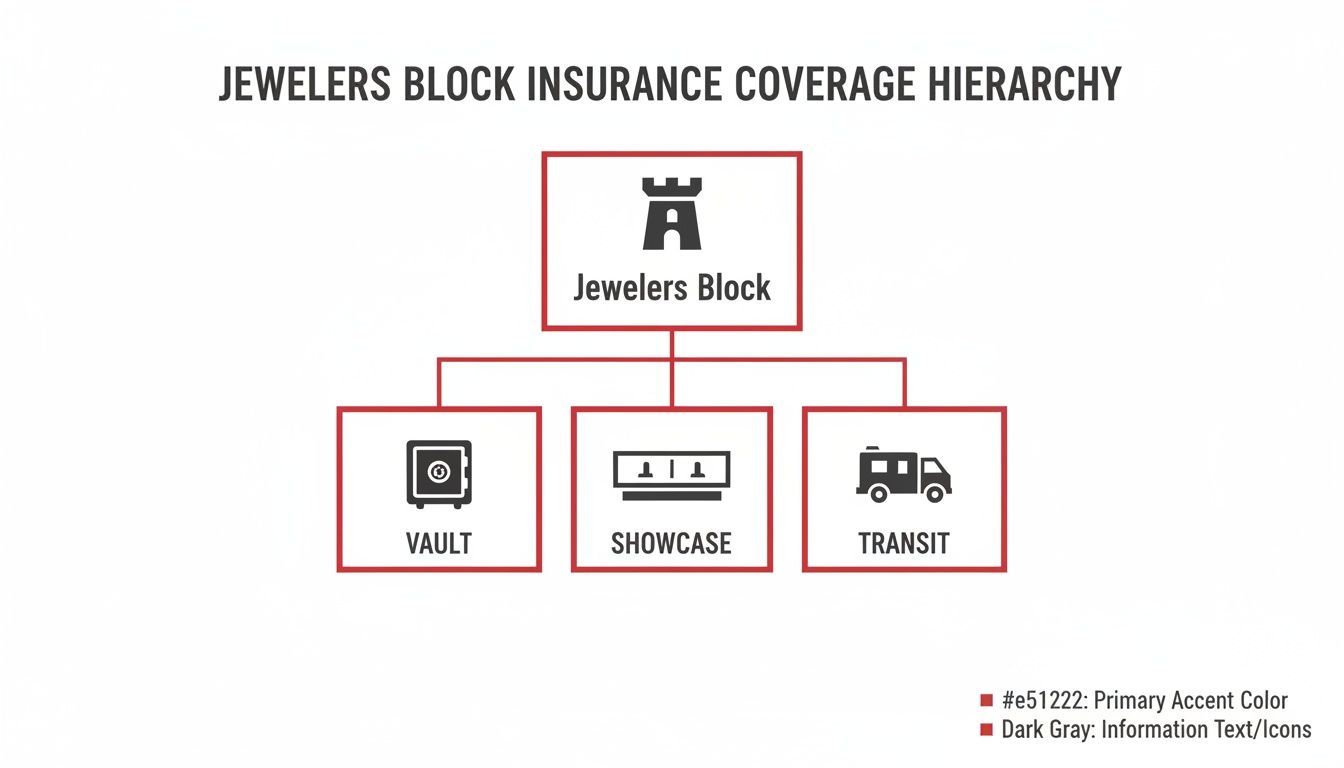

On the other hand, insurance for a jewelry business, known as Jewelers Block insurance, is a whole different ballgame. It's a heavy-duty policy designed to protect everything from the loose diamonds in your safe to the finished pieces in your display cases.

This distinction is everything when it comes to cost. The risks tied to a single ring are worlds apart from those facing a retail store with employees, customers, and a constantly changing inventory. Figuring out which bucket you fall into is the very first step.

A Clear Look at Insurance Costs

To really get a feel for this, think about the scale. A personal policy zeroes in on the retail replacement value of just a few special items. A commercial policy has to cover a massive, dynamic inventory, potential employee dishonesty, and sophisticated security protocols.

Think of it this way: this stunning diamond ring on a black background is what a personal policy protects. For a business, it's just one tiny piece of a much larger, more complex puzzle.

To make it even clearer, here’s a quick breakdown of how the two types of insurance stack up.

Jewelry Insurance Cost At-a-Glance

This table gives you a snapshot of the key differences in annual costs and the factors that drive those premiums for both personal and commercial coverage.

Insurance Type

Typical Annual Cost (as % of Value)

Primary Cost Factors

Personal Jewelry Insurance

1% – 2.5%

Item's appraised value, your location (zip code), and where the item is stored (e.g., home safe vs. bank vault).

Jewelers Block Insurance

0.5% – 1.5%

Total wholesale inventory value, security systems (safes, alarms), business location, and operational procedures.

As you can see, the rates and risk factors are fundamentally different, which makes perfect sense once you understand what each policy is designed to do.

Key Takeaway: While the percentage for personal insurance is higher, the total value being insured is usually much smaller. Conversely, a Jewelers Block policy has a lower rate, but that rate is applied to a massive inventory value, making it a critical line item for any jewelry business.

At the end of the day, whether you need personal protection or comprehensive insurance for a jewelry business, your premium is a direct reflection of risk. Insurers look at everything—from the UL rating on your safe to your claims history—to build a final price. That's why a custom quote is the only way to know for sure what your coverage will cost.

Protecting Your Business with Jewelers Block Insurance

If you're in the jewelry business, you know that a standard, off-the-shelf insurance policy won't even begin to cover you. A generic business owner's policy is like bringing a garden hose to a five-alarm fire—it’s just not built for the unique, high-stakes risks you face every single day.

This is exactly why Jewelers Block insurance exists.

Think of it less as a policy and more as a financial fortress, custom-built to defend your most valuable assets. This specialized insurance for a jewelry business forms a seamless shield of protection. It kicks in the moment new inventory arrives, covers it while secured in your vault, protects it under the bright lights of your showcase, and even follows it when it's in transit to a client or another location.

Why Standard Insurance Fails Jewelers

A regular business policy is designed for common risks, like a customer slipping on a wet floor or damage to your office furniture. It has glaring, expensive gaps when it comes to high-value, portable assets like diamonds, precious metals, and finished pieces.

These standard policies almost always exclude or severely limit coverage for threats that are part of a jeweler's daily reality, including:

Mysterious Disappearance: This is when inventory vanishes without any clear evidence of what happened. It’s a scenario most general policies refuse to touch.

Off-Premises Risks: What happens when your items are away from your store? This covers them at a trade show, with a traveling salesperson, or out for repair.

Theft During Business Hours: This protects you from sophisticated schemes like grab-and-run jobs or distraction thefts that can happen in the blink of an eye.

A Jewelers Block policy is engineered to plug these holes, giving you the wall-to-wall coverage you actually need. It’s the industry standard for a very good reason.

This need for specialized protection is only growing. The global jewelry insurance market was valued at around $4.56 billion in 2023 and is projected to more than double to $9.65 billion by 2033. That surge shows a clear understanding among jewelers that robust, specific coverage is not a luxury—it's essential.

The Comprehensive Shield of a Jewelers Block Policy

What truly sets a Jewelers Block policy apart is its all-in-one nature. Instead of trying to patch together different types of coverage, it bundles them into a single, seamless package. This specialized insurance for a jewelry store is typically underwritten by institutions with deep, firsthand experience in the trade.

One of the key players in this specialized market is Lloyd's of London, which has a long and storied history of insuring unique and high-value risks that other insurers simply won't touch. Their expertise helps shape the kind of rock-solid coverage found in quality Jewelers Block policies.

This type of policy is built on an "all-risk" foundation, which is a critical distinction. It means you're covered for any peril unless it is specifically excluded in the policy. This is the complete opposite of a "named-peril" policy, which only covers the specific risks listed in the fine print, leaving you exposed to everything else.

Ultimately, Jewelers Block insurance is a fundamental risk management tool. It ensures that a single catastrophic event, like a major theft or a fire, doesn't become a business-ending disaster. It provides the financial stability you need to recover, restock, and reopen your doors, preserving the business you’ve worked so hard to build.

Of course, insurance is just one piece of the puzzle. The most successful jewelers also focus on smart operational improvements. You can explore some general strategies to improve your jewellery business that go hand-in-hand with a solid risk management plan.

Key Factors That Shape Your Jewelers Block Premium

Ever wondered why two jewelry stores with similar inventory values can end up with wildly different insurance bills? It’s not random. When you get a quote for Jewelers Block, an underwriter essentially becomes a detective, digging into every aspect of your business to build a precise risk profile.

Knowing what they look for is a huge advantage. It lets you see your business through their eyes and pinpoint exactly where you can make changes that lead directly to savings. The final price you pay for your insurance for a jewelry business is a direct reflection of how well you manage your risk.

This chart breaks down the core pillars of a Jewelers Block policy, showing how it shields your assets whether they're locked away, on display, or on the move.

As you can see, a solid policy acts like a fortress around your inventory, no matter where it is.

Your Inventory's Value and Composition

The biggest driver of your premium, without a doubt, is the total wholesale value of your inventory. That’s the starting point. A store carrying $5 million in stock will naturally have a higher premium than one with $500,000—the potential loss is just that much greater.

But it’s not just about the total dollar amount. The type of inventory you carry is a big deal, too. A stockroom filled with loose, high-value diamonds presents a very different risk than one full of finished silver pieces. Small, high-value items are magnets for thieves, and underwriters know this.

Underwriter's Insight: Insurers focus on your maximum inventory exposure—the highest value your stock hits all year, usually around the holidays. Keeping meticulous, up-to-date inventory records isn't just good practice; it's essential for getting the best possible rate.

The Power of Physical Security Measures

Your security setup is where you can really take control of your premium. Insurers love to see proactive risk management, and nothing says that louder than a top-notch security system. Think of every layer of security as a potential discount on your policy.

It all starts with your safe. Insurers look for specific Underwriters Laboratories (UL) ratings that tell them how well it can resist attacks from tools (TL) and both torches and tools (TRTL). A UL-rated TRTL-30×6 safe, for instance, signals a serious commitment to security and can slash your premium compared to a lower-rated model.

Beyond the safe, your whole security ecosystem comes into play. This includes:

Alarm Systems: A central station-monitored alarm with motion detectors, glass-break sensors, and panic buttons is the industry standard.

Surveillance: High-definition CCTV cameras covering every entrance, showroom, and back office are a powerful deterrent and provide critical evidence if something goes wrong.

Access Control: Systems that log who goes into secure areas and when are crucial for managing internal risks.

When you invest in these systems, you're not just buying equipment. You're making a direct investment in lowering your insurance costs for years to come.

Take a look at how specific upgrades can directly influence what you pay. Each improvement demonstrates to an insurer that you're a lower-risk partner.

How Security Upgrades Impact Jewelers Block Premiums

Security Measure

Description

Potential Premium Impact

Basic Alarm System

A local, unmonitored alarm system.

Baseline

Central Station Alarm

A monitored system that automatically contacts police/fire departments.

5-10% Reduction

Upgraded Safe

Moving from a non-UL-rated safe to a UL TRTL-30×6 rated safe.

15-25% Reduction

HD CCTV System

Comprehensive high-definition camera coverage with remote access.

5-15% Reduction

Access Control

Keycard or biometric systems for secure areas like vaults and back offices.

3-7% Reduction

Showcase Protection

Laminated, smash-resistant glass and secure locking mechanisms.

2-5% Reduction

As the table shows, these aren't just minor tweaks. Making strategic security investments can lead to substantial, long-term savings on your policy.

Location and Operational Risks

Where your store is located makes a big difference for jewelry store insurance. A shop in a quiet suburban area will almost always get a better rate than one in a major city with higher crime stats. Underwriters use geographic data to get a sense of the external threats you face.

But it’s also about what happens inside your four walls. Your day-to-day operations are put under the microscope. Do you have strict rules for showing high-value pieces, like only bringing out one at a time? What are your opening and closing procedures? Do you run background checks on all new hires?

These details are everything. A business with well-documented, strictly followed security protocols is seen as a much safer bet than one that's more relaxed. Every single procedure that cuts down the odds of a loss helps you build a case for a lower premium.

Finally, your claims history is your track record. A business with few or no claims over the years proves it has a handle on risk and will likely be rewarded with better rates. On the flip side, a history of frequent claims signals higher risk and will almost certainly mean a higher premium. By understanding these factors, you can make strategic choices that not only protect your business but also boost your bottom line.

Understanding Personal Jewelry Insurance Costs

While Jewelers Block insurance is designed to protect a business, personal jewelry insurance is all about safeguarding your own individual treasures. Whether you're insuring a new engagement ring, a luxury watch, or a beloved collection of valuable antique jewelry, the underlying logic is the same: the cost is based on risk.

But for a personal policy, the risks look a little different than they do for a retail store. Here, the insurance company isn't looking at your display cases and employee protocols. Instead, they’re focused on your personal habits, where you live, and the specific pieces you own.

Key Factors Driving Your Personal Premium

Just like with a commercial policy, a few key things will determine your rate. The single biggest factor is the official appraised value of your jewelry. It’s absolutely vital that this appraisal is recent—we recommend getting it updated every two to three years—to keep up with the fluctuating market for gold, platinum, and gemstones. Relying on an old appraisal is a surefire way to find yourself underinsured.

Where you live also makes a huge difference. Insurers look closely at crime statistics in your zip code. Someone living in a quiet, low-crime suburb will almost always pay less than a person in a dense urban center where theft is more common.

Finally, your storage habits are critical. Keeping a high-value item in a bank safety deposit box is the gold standard for security and can earn you some serious discounts. The next best thing is a quality, UL-rated home safe. Simply stashing your heirlooms in a dresser drawer, on the other hand, represents the highest risk and will absolutely lead to a higher premium.

Crucial Choice: A dedicated, standalone jewelry policy offers far superior protection compared to a simple rider on a homeowners policy. Standalone policies often cover risks like "mysterious disappearance"—when an item vanishes without evidence of theft—which is a common exclusion on standard homeowners coverage.

To get an accurate handle on your potential costs, you first need to establish the real value of your items. This often means getting professional verification, like following guides on authenticating valuable luxury watches.

Real-World Cost Examples for Personal Jewelry

Seeing some numbers can help put all this into perspective. Let’s walk through a few common scenarios, assuming a standard deductible and a mid-range risk location.

A $10,000 Engagement Ring: For a ring at this value, you can generally expect an annual premium between $100 and $200. The final number will move up or down depending on your specific zip code and how securely you store it.

A $5,000 Luxury Watch: A watch in this price range typically costs about $75 to $150 per year to insure. Watches have a slightly different risk profile than rings, which is reflected in the premium.

A $25,000 Necklace: When you get into higher-value pieces like this, the premium might range from $250 to $500 annually. At this level, proving you use secure storage, like a home safe, becomes a major factor in keeping your costs reasonable.

It’s no surprise that so many people choose to protect their valuables. In fact, the United States accounts for a massive 26% of the global jewelry insurance market share, showing just how important proper coverage is to American consumers.

Actionable Strategies to Lower Your Insurance Premiums

While the cost of jewelry insurance is a necessary business expense, it’s not a number that’s set in stone. By taking proactive steps to manage and reduce your risk, you can have a direct impact on the premium you end up paying. These strategies aren't just about saving money—they're smart operational practices that underwriters actively reward.

When you implement robust security and meticulous protocols, you're showing a serious commitment to protecting your assets. That makes you a much more attractive client to insurers. This is where you shift from simply reacting to risk to actively controlling it, and that control translates into tangible savings on your jewelry store insurance.

Fortifying Your Business for Premium Reductions

For jewelry business owners, the most significant savings come from strategic investments in both physical and procedural security. Think of your store as a fortress; the stronger your defenses, the lower the perceived risk.

Upgrading your safe is one of the most powerful moves you can make. Swapping a basic safe for a high-security, UL-rated TRTL-30×6 safe can lead to premium reductions of 15-25%. It’s a crystal-clear signal to insurers that your highest-value assets are exceptionally well-protected against even the most sophisticated attacks.

Beyond the vault, a comprehensive security system is essential. This includes:

Advanced CCTV: High-definition cameras covering every angle not only deter criminals but also provide invaluable evidence if an incident ever occurs.

Central Station Alarms: A system monitored 24/7 by a professional security firm ensures a rapid response to any breach, which can dramatically reduce the potential for a major loss.

Rigorous Protocols: Documented procedures for opening, closing, and showing high-value items are critical. Simple rules, like showing only one high-value piece at a time, drastically lower the risk of a grab-and-run theft.

By implementing these measures, you are not just buying equipment; you are investing in a lower premium for your insurance for jewelry business.

Smart Tactics for Personal Collections

For individuals protecting personal jewelry, similar principles apply, just on a smaller scale. The choices you make about storage and security have a direct impact on your insurance costs.

The single most effective way to lower your premium is by storing items you don't wear frequently in a bank's safety deposit box. It is the ultimate secure environment, and insurers reward this decision with substantial discounts because the risk of theft is nearly eliminated.

For the pieces you do keep at home, a quality home security system and a properly installed home safe can also lead to meaningful savings. Just as with a commercial policy, demonstrating that you take security seriously helps prove you are a low-risk client. Taking these steps is the key to securing better rates while making sure your treasures remain protected.

Get the Right Coverage with a Custom Quote

After breaking down all the moving parts that go into an insurance premium, one thing should be crystal clear: there's no such thing as a "standard price" in the world of jewelry insurance. The only real way to know how much jewelry insurance will cost for your collection or your business is to get a quote built from the ground up.

Every policy is a direct reflection of a unique risk profile. So, instead of relying on ballpark estimates, a custom quote from a specialized Jewelers Block agency like First Class Insurance gives you the clarity you actually need. We dig into your inventory, your security measures, your location, and your day-to-day operations to build a policy that fits just right—ensuring you're not overpaying for coverage you don't need or leaving yourself exposed with dangerous gaps.

Tailored Protection for a Growing Market

The need for precise, expert-driven coverage has never been more critical. The global jewelry market was valued at around $232.94 billion in 2024 and is expected to rocket to $343.90 billion by 2032. This incredible growth means more businesses and individuals are looking to protect incredibly valuable assets, making specialized insurance less of a luxury and more of a necessity. You can see more data on this expanding market over at fortunebusinessinsights.com.

At First Class Insurance, we don't believe in one-size-fits-all policies. We know the needs of a wholesale diamond dealer are worlds apart from a private collector's. As a dedicated Jewelers Block Agency, our entire process is designed to deliver a straightforward, comprehensive quote that aligns perfectly with your specific risks and your budget.

Your Path to a Clear and Accurate Quote

Stop guessing what your insurance for a jewelry store might cost. With over 30 years of experience, our team at First Class Insurance specializes in building customized Jewelers Block policies for businesses all across the country. We also craft dedicated personal policies for collectors with significant, high-value pieces.

The process is simple. Let our experts analyze your needs and deliver a clear, no-obligation quote, often within 24 hours. Connect with our team today to secure the precise protection your assets demand. Real peace of mind starts the moment you get a quote for Jewelers Block and see just how affordable true security can be.

Common Questions About Jewelry Insurance

Diving into the world of jewelry insurance, whether for your business or a personal treasure, always brings up a few key questions. Let's clear up some of the most common things people ask, so you can feel confident you're getting the right protection.

Think of this as the practical advice you need to navigate the fine print.

Is Jewelers Block Insurance Required by Law?

Here's the short answer: no, Jewelers Block insurance isn't typically mandated by law. But in the real world of the jewelry industry, it’s absolutely essential. You simply can't operate a serious business without it.

Why? Because the third parties you rely on will demand it. Your landlord, your bank, and even the suppliers you work with will often have contractual requirements for you to carry proper coverage. They need to know that a major loss won't put you—and by extension, them—out of business. Trying to run a jewelry store without it is a gamble no professional is willing to take.

What Is the Difference Between Appraised and Wholesale Value?

This is one of the most important distinctions, and it separates personal coverage from commercial.

Appraised value is the full retail replacement cost. It's the price tag a customer would see in a store, and it’s the number used to insure a personal item on a homeowner's policy.

Wholesale value, however, is what it actually cost you to create or acquire the piece—the price of the metal, the gems, and the labor. This is the value a Jewelers Block agency uses to insure your business inventory. Commercial policies are designed to make you whole on your investment, not cover your potential profit margin.

Will a Single Claim Dramatically Increase My Premium?

Not necessarily. It really depends on the story behind the claim. Insurers are looking at the whole picture—the type of claim, how severe it was, and your history.

A small, one-off incident might only cause a minor bump in your rate. This is especially true if you can show you've taken clear steps to prevent it from happening again. On the other hand, a pattern of claims or a single catastrophic loss will almost certainly lead to a more significant rate increase.

Expert Insight: This is where working with a specialist agent really pays off. When you file a claim, they can help you present it to the underwriter in the best possible light and advise you on risk management to minimize the long-term impact on your premiums.

How Often Should I Reappraise My Jewelry?

For personal jewelry, you should get a professional reappraisal every two to three years. The values of precious metals and gems fluctuate constantly. An appraisal from five years ago could leave you seriously underinsured if you have to file a claim today.

It's a different story for a commercial insurance for jewelry business policy. Your Jewelers Block coverage is based on your current wholesale inventory, which you should be tracking continuously anyway. As long as your records are up-to-date, your coverage will automatically align with the real-time value of your stock.

The world of jewelry insurance has its own rules and language, but you don’t have to figure it all out on your own. At First Class Insurance, our specialists live and breathe this stuff. As a leading Jewelers Block Agency, we're here to answer your questions and build a policy that fits your business or collection perfectly.

Get the peace of mind that comes from knowing your most valuable assets are properly protected. Visit us at https://firstclassins.com to get your custom quote today.

{kind=link}

{kind=link}