For a jewelry store owner, insurance isn't just about checking a box for compliance—it's about survival. You’ll have legal requirements, sure, like Workers' Compensation if you have employees and General Liability to satisfy your landlord. But the real make-or-break coverage for a jeweler comes from protecting the very things that make your business unique: high-value, portable inventory.

What Insurance Is Required for a Jewelry Business

Let's break down insurance into two distinct layers. Think of it as the legal foundation you have to build, and then the specialized shield that actually protects what's most valuable.

The legal foundation covers the basics that nearly every small business needs. If you have even one employee, almost every state mandates Workers' Compensation. It’s non-negotiable. This policy handles their medical bills and lost income if they get hurt on the job. Likewise, your lease agreement will almost certainly demand General Liability insurance to cover things like a customer slipping and falling in your store.

Beyond the Basics for Your Jewelry Store

Here’s the problem: those foundational policies leave your most valuable assets—your diamonds, gold, and finished pieces—dangerously exposed. A standard property policy is simply not built for the realities of the jewelry world. It often has absurdly low limits for theft and completely ignores the unique risks you face every single day.

This is where your specialized shield comes in. For anyone serious about this business, Jewelers Block insurance isn't just a good idea; it's a fundamental requirement. It’s an all-risk policy designed from the ground up to protect your inventory from a huge range of threats.

Think of it like a bank vault. The law might require a basic fire alarm, but the real security comes from the reinforced steel door. Standard business policies are the alarm, but a Jewelers Block policy is the vault door that truly protects your assets.

Building Your Protective Shield

A proper insurance plan for a jeweler has to cover risks other policies won't even touch. This specialized coverage is designed to protect your inventory whether it's locked in the safe, sitting in a showcase, or even being shipped to a trade show. It’s what closes the critical gaps left by one-size-fits-all insurers.

The table below gives you a quick snapshot of the policies you’ll encounter, separating the non-negotiable requirements from the essential recommendations that protect your livelihood.

Required vs. Recommended Insurance for Your Jewelry Store

| Insurance Type | Typically Required By | Primary Purpose for a Jeweler |

|---|---|---|

| Workers' Compensation | State Law (with employees) | Covers employee injuries, protecting you from lawsuits and fines. |

| General Liability | Commercial Leases | Protects against third-party claims like customer slip-and-falls. |

| Commercial Auto | State Law (for business vehicles) | Covers liability and damage for vehicles used for business purposes. |

| Jewelers Block | Strongly Recommended | The core policy; provides all-risk coverage for your entire inventory. |

| Professional Liability | Contracts (sometimes) | Protects against claims of negligence, like a faulty appraisal. |

| Surety Bonds | Government/Contracts | Guarantees you will fulfill a specific obligation (e.g., customs bond). |

Navigating these unique needs is what an expert agency does best. At a dedicated First Class Insurance Jewelers Block Agency, our entire focus is on your industry. We help you build a policy that secures everything you've worked for.

Ready to protect your assets? Get a Quote for Jewelers Block to see how a policy built for a jeweler can safeguard your business.

The Foundation of Business Insurance Coverage

Every business, no matter the industry, needs a solid layer of protection to stand on. Think of it like building a house. Before you can even think about installing custom vaults and high-tech security for your valuables, you have to pour the concrete foundation and put up the walls. For any business—and especially a high-end jewelry store—these foundational insurance policies are the essential structure holding everything else up.

So, let's break down the four cornerstones of small business insurance. These policies are designed to handle the most common risks that nearly every company runs into, from a customer slipping on a wet floor to an employee getting injured on the job. They are absolutely critical, but it's just as important to understand where their protection stops.

General Liability Insurance

People often call this "slip-and-fall" insurance, and for good reason. General Liability is your first line of defense against claims from third parties for bodily injury or property damage. If a customer trips over a display rug in your showroom and breaks their wrist, this policy is what covers their medical bills and your legal fees. It's the most common coverage out there and is often a non-negotiable part of a commercial lease before you can even get the keys.

Commercial Property Insurance

While general liability protects you from claims by others, Commercial Property insurance is all about protecting your own physical stuff. This policy is designed to repair or replace your business property if it's hit by things like a fire, a major storm, or a break-in. For a jewelry store, that means covering things like:

- The building itself (if you own it)

- Your display cases, custom lighting, and furniture

- Computers, point-of-sale systems, and back-office equipment

- Security systems and safes

But here’s the catch, and it's a big one. A standard commercial property policy has shockingly low limits for high-value items like jewelry. This is precisely why specialized insurance for a jewelry business isn't just a good idea—it's essential.

Workers' Compensation Insurance

If you have employees, Workers' Compensation isn't optional. It's legally required in almost every single state. This policy is a fundamental agreement between you and your team. It covers their medical bills and a portion of their lost wages if they get hurt or sick as a direct result of their job. In exchange, it generally protects you from being sued by that employee.

This coverage isn't a suggestion; it's the law. Trying to operate without it can bring on crushing fines, penalties, and even criminal charges, making it one of the most critical small business insurance requirements you have to meet.

Commercial Auto Insurance

Finally, if you or your staff use a vehicle for anything business-related, your personal auto policy won't touch it. Whether it's a dedicated delivery van or just your personal car used for bank runs and errands, you absolutely need Commercial Auto insurance. This policy covers liability and physical damage if an accident happens while you're on the clock.

These four policies create a solid base, but far too many business owners stop here, leaving themselves dangerously exposed. Despite growing revenues, underinsurance is a massive problem. The 2025 Hiscox Underinsurance in Small Business Report found that a staggering 77% of U.S. small businesses are underinsured. The gaps are huge—only 65% have general liability, and just 49% carry property insurance. You can dig into the complete findings on underinsurance trends to see the risks for yourself.

These foundational policies are vital, but for a jeweler, they leave your most valuable asset—your inventory—almost completely unprotected. This is exactly why specialized coverage, the kind we build with expert underwriters from places like Lloyd's of London, isn't just a recommendation. It's a requirement for survival.

{kind=link}

Why Jewelers Block Is Your Most Important Policy

The standard business policies we’ve already walked through are built for a world of office furniture, clothing racks, and restaurant grills. Let’s be blunt: they are fundamentally unprepared for the realities of the jewelry business.

This is where Jewelers Block insurance comes in—not as some optional add-on, but as the absolute cornerstone of your entire protection strategy.

Think of it this way. A standard commercial policy is like a generic, off-the-rack jacket. It offers basic protection but fits poorly and leaves massive gaps. A Jewelers Block policy, on the other hand, is a custom-tailored suit of armor, designed from the ground up to protect your most valuable and vulnerable assets. It is, without question, the single most important piece of insurance for a jewelry store.

This specialized policy is built to wrap multiple coverages into one seamless package, designed to follow your inventory no matter where it goes. It’s written as an "all-risk" policy, which means it covers every imaginable threat unless a peril is specifically excluded in the fine print.

The All-In-One Shield for Your Inventory

Unlike the foundational policies that carve out separate coverage for your building, your liability, and your inventory, a Jewelers Block policy is built around your most critical asset: the jewelry itself. It protects your entire stock—from loose diamonds and raw metals to finished pieces—against a whole range of threats that standard policies just weren't designed to handle.

This comprehensive approach is exactly what makes it so vital. Your inventory is protected whether it is:

- Secured in your safe overnight. This is the most basic layer of protection, covering your items when they’re locked away.

- On display in your showroom during business hours. This covers the immense risk that comes with having high-value items visible and accessible.

- Being worked on by a bench jeweler. The policy extends to pieces that are in the process of being created, repaired, or altered.

- In transit to a trade show or another location. One of the biggest holes in standard coverage is off-premises protection; Jewelers Block closes that gap completely.

- With a salesperson visiting a client. Coverage follows your inventory even when it’s in the hands of your trusted team outside the store.

This all-encompassing protection is a game-changer for any insurance for jewelry business. It’s built for the real-world situations you face every single day.

A standard policy might cover a fire, but what about a skilled thief who swaps a real diamond for a fake one? Or a package that simply vanishes in transit? Jewelers Block is built for these specific, high-stakes scenarios. It’s not just a policy; it’s a business survival tool.

Covering Perils Others Exclude

The true power of a Jewelers Block policy is in the unique risks it covers. Standard property insurance is notorious for its laughably low sub-limits on theft, especially for items like jewelry. A typical policy might cap theft coverage at a mere $2,500—an amount that wouldn't even cover a single decent engagement ring.

Worse, these policies are riddled with exclusions that are catastrophic for a jeweler. A Jewelers Block policy, however, is designed to specifically cover these high-risk events.

Key Coverages in Jewelers Block Insurance

| Peril Covered | Why It's Critical for a Jeweler |

|---|---|

| Armed Robbery & Burglary | Provides robust coverage for losses during a hold-up or a sophisticated break-in, far exceeding standard policy limits. |

| Mysterious Disappearance | Covers inventory that is lost or missing without a clear explanation of what happened—a common and frustrating scenario. |

| Employee Dishonesty | Protects your business from the significant financial damage caused by internal theft, a risk often overlooked. |

| Travel & Transit Risks | Insures your inventory while you're traveling to trade shows, visiting clients, or shipping items to customers. |

At a specialized First Class Insurance Jewelers Block Agency, our entire focus is on crafting these policies. We understand that your inventory's security is directly tied to your physical security measures. To protect your valuable inventory, consider implementing robust high security solutions as a crucial part of securing your assets, directly influencing the scope and cost of your Jewelers Block policy.

These specialized policies are the core of meeting your true small business insurance requirements. They are not an optional upgrade; they are an absolute necessity. To truly understand how this coverage can be shaped to fit your unique operations, the best next step is to Get a Quote for Jewelers Block from an expert who knows your industry inside and out.

Covering Your Unique Industry Risks

While a Jewelers Block policy is the powerful centerpiece of your protection, a truly secure jewelry business layers specialized coverage on top to handle specific, high-stakes threats. Think of it like adding reinforced walls and advanced surveillance to your vault. Each additional policy closes a specific loophole, creating a comprehensive shield that anticipates the real risks you face every day.

This is a critical step in meeting your true small business insurance requirements. It's about moving beyond the basics to build a plan that can withstand the unexpected. Let's dig into the essential riders and standalone policies that every owner of an insurance for a jewelry business should have on their radar.

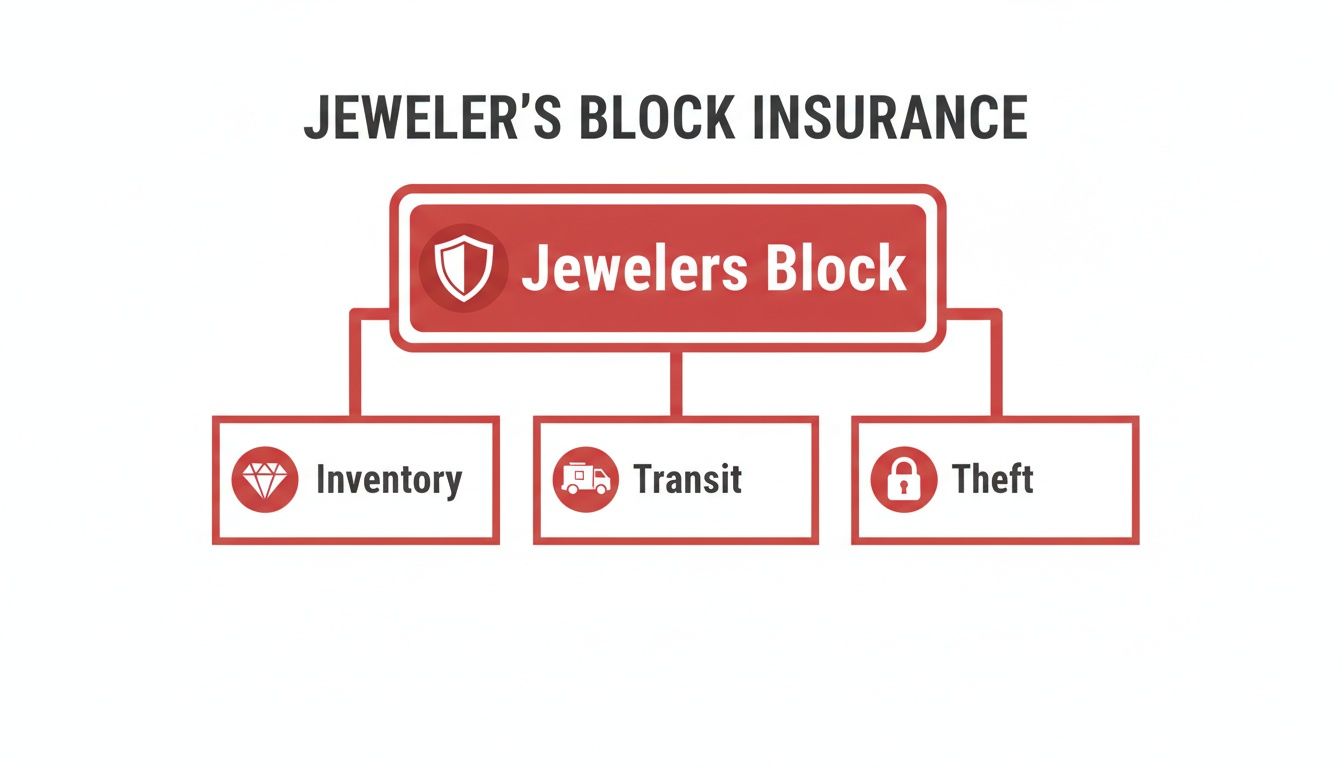

This diagram shows how a Jewelers Block policy acts as the core, branching out to protect your key assets across inventory, transit, and theft.

As you can see, a single, robust policy is designed to be the foundation of your security strategy, protecting your assets no matter where they are.

Employee Dishonesty Coverage

Let's be honest—one of the most sensitive but significant threats to a jewelry business comes from within. Employee theft is a massive source of loss in our industry, often happening subtly over a long period. Standard policies almost never cover internal theft, making Employee Dishonesty coverage absolutely essential. This protects your business from financial losses due to fraudulent acts committed by an employee.

Transit and Shipping Insurance

Your inventory is never more vulnerable than when it's on the move. Whether you're shipping a high-value piece to a client, sending items to a trade show, or receiving a new collection, dedicated Transit Insurance is vital. While Jewelers Block offers some transit protection, a specialized policy gives you higher limits and broader coverage for both domestic and international shipments, ensuring your assets are protected door-to-door.

Mysterious Disappearance is a crucial part of specialized jeweler coverage. It protects you from inventory losses that can't be explained by a specific event—like a ring that is simply gone from a display case at the end of the day with no evidence of theft. Standard policies won't touch this.

Cyber Liability Insurance

As more sales move online and client data is stored digitally, your business becomes a prime target for cybercriminals. Cyber Liability insurance is no longer a "nice-to-have"; it's a critical safeguard. It protects you from the crippling costs of a data breach, including notification expenses, credit monitoring for affected clients, and hefty legal fees.

The risk is real and growing. It's shocking, but only 31% of small and medium-sized businesses carry cyber insurance, yet a staggering 57% have already suffered a breach. For a jeweler, the threat goes beyond stolen credit card numbers to include digital inventory lists or sensitive client information, making this coverage more critical than ever.

The following table breaks down why a standard business policy just doesn't cut it for the unique risks jewelers face.

Standard vs. Specialized Jeweler Insurance

| Risk Scenario | Standard Commercial Property/Liability | Jewelers Block & Specialized Riders |

|---|---|---|

| A ring vanishes from a display case overnight. | Not Covered. Lacks proof of forced entry or a specific insured event. | Covered. This is a classic "mysterious disappearance" scenario. |

| An employee steals several small diamonds over six months. | Not Covered. Employee theft is a specific exclusion in most standard policies. | Covered. An Employee Dishonesty rider is built for this exact situation. |

| An armored carrier shipment is hijacked. | Limited or No Coverage. Coverage often ends once property leaves your premises. Carrier liability is minimal. | Covered. Transit insurance provides seamless, door-to-door protection. |

| A customer's watch is damaged during repair. | Not Covered. Standard liability typically excludes "care, custody, or control" of customer property. | Covered. This is protected under the policy's bailee coverage. |

As you can see, relying on general commercial insurance leaves dangerous gaps that specialized policies are designed to fill.

Enhancing Physical Security Protocols

Your insurance coverage and your physical security are deeply intertwined. Insurers will always look at your security measures—safes, alarms, surveillance—when setting your premiums. Taking proactive steps to secure your premises not only deters criminals but can also lead to much better insurance terms. For instance, knowing how to change the combination on a safe and doing it regularly is a simple protocol that underwriters love to see.

By layering these specialized coverages, you create a security net that addresses the full spectrum of risks in the jewelry trade. From protecting your precious antique jewelry (https://jewelersblockins.com/wp-content/uploads/2025/11/antique-jewelry-scaled-1-768×512.jpg) to securing your digital storefront, each policy plays a vital role in keeping your business whole.

{kind=link}

Figuring Out What Insurance You Actually Need

Let’s be honest, figuring out insurance can feel like a chore. But for a jeweler, it's not a guessing game—it's about building a fortress around your life's work. The whole point is to move beyond just checking a box and get the real protection you need.

The absolute starting point, the foundation of it all, is a meticulous inventory valuation. You have to know the exact dollar value of everything you hold: loose stones, finished pieces, customer repairs, and even raw materials. This number is the bedrock of your Jewelers Block insurance policy.

Once you have that figure, you need to tackle your legal and contractual obligations. These aren't suggestions; they're the non-negotiable insurance requirements others place on you.

What Coverage Are You Forced to Carry?

Before we get to protecting your diamonds and gold, you have to satisfy the demands of landlords and the law. Think of this as the mandatory groundwork for your entire insurance plan.

First, pull out your commercial lease agreement and read the insurance section carefully. Landlords almost always require specific limits for General Liability and Commercial Property insurance. If you don't meet their minimums, you're in breach of your lease—it's as simple as that.

Next up is workers' compensation. If you have employees, your state almost certainly requires you to have it. The rules and required coverage amounts can vary wildly from one state to another, so you absolutely must check your local laws.

How to Calculate Your Ideal Coverage

With the mandatory stuff out of the way, you can focus on what really matters: protecting the core of your business. This is where you figure out the coverage limits that will let you get back on your feet after a total disaster.

And here’s a critical point: it’s not about what you paid for everything. It's about what it would cost to replace it all today.

This is the huge difference between 'replacement cost' and 'actual cash value.' You need a policy that gives you enough money to rebuild your store and restock your entire inventory at today's market prices, not their old, depreciated value. For any insurance for a jewelry store, this distinction is everything.

The global market for small business insurance is exploding for a reason. It was valued at $17,501 million in 2021 and is projected to rocket to $28,673.1 million by 2033. This isn't just a random number; it shows that business owners everywhere are waking up to how vital proper protection is, especially for jewelers sitting on high-value assets. You can discover more insights about this expanding market to see why specialized coverage is no longer optional.

A classic mistake is insuring your inventory for what you paid for it years ago. If a fire wipes you out, you need enough cash to replace everything at today's wholesale prices, which could be dramatically higher.

This is where working with a specialist pays for itself. An expert from a dedicated First Class Insurance Jewelers Block Agency lives and breathes the valuation methods unique to the jewelry industry. We can help you build a truly custom strategy that protects your business from every angle. Don't leave your livelihood up to chance.

To start building your shield, Get a Quote for Jewelers Block today.

Get Your Custom Jewelers Block Quote

All this talk about risk is one thing, but turning that knowledge into real protection is what actually matters. Protecting your livelihood with the right jewelry store insurance doesn't have to be some long, drawn-out ordeal. Here at First Class Insurance Jewelers Block Agency, we’ve built our entire business around making this critical step simple for jewelers who have better things to do.

Getting a quote is probably easier than you think. We take the mystery out of the process by walking you through exactly what we need to build a policy that fits your business like a glove—no frustrating guesswork involved.

Information Needed for Your Quote

To put together an accurate quote, an insurance specialist just needs a few key details about how you operate. Having this info ready makes everything go much faster.

You should have this on hand:

- Current Inventory Value: The total replacement cost for everything you have in stock. That includes loose stones, finished pieces, and even customer items in for repair.

- Security System Details: Tell us about your safes (especially their UL rating), alarm systems, and cameras. Better security almost always means better premiums. It’s that simple.

- Business History: Just the basics, like how long you’ve been in business and any claims history you might have.

- Operational Scope: A quick rundown of what you do—retail, wholesale, manufacturing, trade shows, etc.

Securing the right jewelry store insurance is the final, most critical step in safeguarding your hard work. It transforms your knowledge of risks into a tangible shield, providing the peace of mind needed to focus on growing your business.

At First Class Insurance, we’ve designed our process specifically for the jewelry trade. Our goal is to get a detailed quote back to you, often within 24 hours, so you can make a smart decision without delay. To see the kinds of high-value pieces we protect every day, just look at this stunning diamond ring on a black background.

{kind=link}

Don’t leave your life’s work exposed for another minute. It’s time to partner with an expert who knows your industry inside and out—someone who can build the right policy to protect your inventory, your reputation, and your future.

Common Questions Jewelers Ask About Insurance

When you're dealing with small business insurance requirements, it's easy to get lost in the details. Let's cut through the noise and tackle the questions we hear most often from jewelers, giving you the straightforward answers you need to protect your business.

Jewelers Block vs. Standard Insurance: What's the Real Difference?

The biggest difference is specialization—and in this business, that's everything. A standard commercial policy is a generic, off-the-shelf product built for an average Main Street business. The problem? It often comes with dangerously low theft limits and simply ignores the unique risks you face every single day.

A Jewelers Block insurance policy, on the other hand, is built from the ground up specifically for your trade.

It's a comprehensive policy designed to cover your high-value inventory against a whole universe of risks that standard policies won't even consider. We're talking about things like shipping to a customer, traveling to a show, or even the dreaded mysterious disappearance. Think of it as a custom-tailored suit of armor versus a one-size-fits-all rain poncho.

How Much Does Insurance for a Jewelry Business Actually Cost?

There's no flat rate for insurance for a jewelry business because every jeweler's risk profile is completely different. The final premium is a unique number calculated based on the specific details of your operation.

Insurers are going to look closely at a few key things:

- Your Total Inventory Value: It's simple—the more your collection is worth, the more coverage you need.

- Your Physical Location: The store's neighborhood and local crime statistics absolutely play a role.

- Your Security Measures: This is where you have control. A top-tier safe, advanced alarms, and full-coverage surveillance can earn you some serious discounts.

- Your Claims History: A clean track record without prior losses will always get you a better price.

Because of all these moving parts, the only way to find out your true cost is to have an expert take a hard look at your specific setup.

A common mistake is thinking all policies are priced the same. The truth is, your investment in top-notch security, like a UL-rated TRTL-30×6 safe, directly translates into lower, more manageable insurance premiums. Insurers love to see that you're taking risk seriously.

Am I Covered When I Travel to Trade Shows?

Yes, but only if you have the right policy. Your standard business owner's policy will almost certainly stop protecting your inventory the second it leaves your storefront. This is one of the most critical gaps that specialized jewelry store insurance is designed to fill.

A true Jewelers Block policy is built with "off-premises" and "in-transit" coverage baked right in. That means your inventory is protected while you’re on the road to a trade show, visiting a private client, or attending any other industry event. It’s a seamless shield that follows your assets wherever your business takes you.

Your business is built on trust and incredibly valuable assets. You can't afford to leave its safety to a generic policy that wasn't made for you. At First Class Insurance, we're a dedicated agency that lives and breathes the unique risks of the jewelry world. Let our experts build a policy that truly secures your inventory, your reputation, and your peace of mind.

Get your custom quote today by visiting us at https://firstclassins.com.