When you’re shipping high-value jewelry, your standard business policy just won’t do. Real protection for your assets on the move comes from a specialized type of coverage: marine and cargo insurance. This is a critical component of a comprehensive Jewelers Block insurance policy.

Think of it as a personal security detail that guards your inventory from the moment it leaves your hands until it’s safely signed for, whether it’s crossing an ocean or just the state line.

Why Your Jewelry Needs Specialized Transit Insurance

For any jeweler, inventory is everything. Whether you're sending a finished piece to a client, getting diamonds from an overseas supplier, or just moving stock between stores, every single shipment carries immense value.

A standard business or property policy is full of holes when it comes to covering goods once they’ve left your building. This is exactly where marine and cargo insurance, as part of your overall insurance for jewelry business, becomes a non-negotiable part of your risk management.

The unique dangers of shipping precious metals and gems demand coverage that goes way beyond a typical policy. Standard carriers often cap their liability at a tiny fraction of a shipment’s real worth—sometimes as low as $100 per package. Relying on that is a gamble you simply can't afford with one-of-a-kind items.

Addressing the Unique Risks of High-Value Shipments

The journey a piece of jewelry takes is filled with threats that generic policies were never built to handle. A smart insurance plan for a jewelry store has to account for these specific transit weak spots.

Here’s why you absolutely need specialized coverage:

- High Target for Theft: Jewelry is small, valuable, and easy to carry, making it a top target for organized crime rings that specialize in hitting cargo in transit.

- Mysterious Disappearance: It’s the stuff of nightmares—a package arrives with its seals intact, but the contents are gone. This kind of loss is often excluded from basic policies but can be covered under a well-designed marine policy.

- Damage and Mishandling: Delicate settings and precious stones can be easily damaged by rough handling, temperature swings, or simple accidents during shipping.

- Global Supply Chain Complexity: International shipments bring a whole new set of risks, from customs delays that leave goods vulnerable to piracy and political unrest.

A robust Jewelers Block policy isn't just for your storefront; it's a comprehensive shield that extends to your inventory in motion. First Class Insurance ensures that marine and cargo coverage is seamlessly built in, giving you true vault-to-vault protection.

At the end of the day, this specialized coverage makes sure your financial interests are protected from the unpredictable world of logistics. For a better sense of what’s at stake, you can see examples of the luxury timepieces and jewelry that require this level of dedicated insurance. Protecting these assets is fundamental to your business's stability and reputation.

{kind=link}

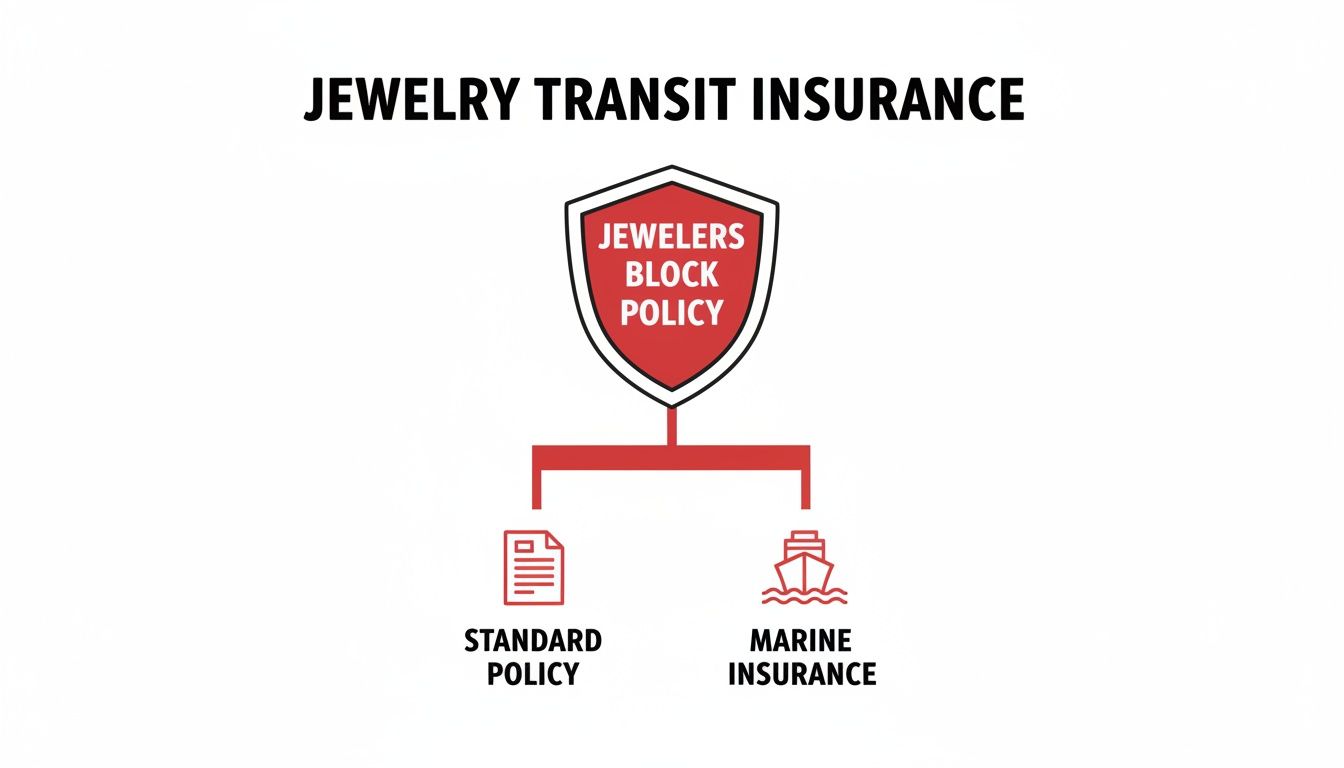

Understanding Ocean vs. Inland Marine Insurance

When you hear "marine insurance," it’s easy to get lost in the jargon. But for any jewelry business, getting a handle on the two core types—Ocean Marine and Inland Marine—is non-negotiable. These aren't just technical terms; they are the specific shields that protect your high-value inventory as it moves from one place to another.

Think of it like this: Ocean Marine insurance is the guardian of your international shipments, while Inland Marine insurance protects everything moving within a country's borders. For a jeweler importing diamonds, exporting custom pieces, and shipping to domestic clients, you absolutely need both as part of your jewelry store insurance.

This breakdown shows how a well-built Jewelers Block policy is structured, integrating specialized transit coverage like marine insurance right alongside your standard protections.

As you can see, a standard policy is just the base. True peace of mind comes from layering on specialized marine insurance, which is a vital part of a top-tier Jewelers Block policy.

Ocean Marine Insurance: Your Global Shield

Ocean Marine is the oldest form of this protection, originally designed to cover goods traveling across the high seas. Today, it covers assets moving by water or air between countries. This policy kicks in when you’re importing diamonds from Antwerp, sending a bespoke necklace to a client in London, or receiving a shipment of watches from Switzerland.

It's built to handle the unique risks of international voyages, including:

- Perils of the Sea: Protection against losses from things like massive storms, sinking, or collisions.

- Theft and Piracy: A very real threat in certain shipping lanes that your standard policy would never touch.

- Container Mishaps: Coverage if the shipping container is damaged, lost overboard, or mishandled at a busy port.

- General Average: A fascinating maritime principle where all parties in a sea voyage proportionally share any losses from a voluntary sacrifice (like jettisoning cargo) made to save the entire venture in an emergency.

Navigating the complex details on international shipping is a huge undertaking, and a misstep here can leave catastrophic gaps in your coverage.

Inland Marine Insurance: The Domestic Guardian

Despite the name, Inland Marine insurance has very little to do with water. The name is a holdover from when it was created to cover goods after they were offloaded from a ship and began their journey "inland." Today, it’s the essential coverage for any valuable property that is mobile and moving over land.

For a jewelry store, this is your everyday transit protection. It covers a tray of rings being sent between your stores, inventory heading to a trade show in Las Vegas, or a finished engagement ring being shipped to a customer one state over. It protects against risks like truck accidents, theft from a delivery vehicle, or damage during loading and unloading. Its roots are deep, involving specialized markets and entities like https://jewelersblockins.com/wp-content/uploads/2025/11/lloyd-s-of-london-logo-463×38-1-1-300×115.jpg that pioneered this kind of modern coverage.

{kind=link}

Let’s break down where each policy comes into play with a simple comparison.

Ocean Marine vs Inland Marine: A Jeweler's View

| Coverage Aspect | Ocean Marine Insurance | Inland Marine Insurance |

|---|---|---|

| Primary Scope | International transit (sea, air) | Domestic transit (land, domestic air) |

| Typical Scenario | Importing diamonds from India. | Shipping a ring to a customer in another state. |

| Key Risks Covered | Piracy, storms at sea, container loss. | Vehicle accidents, cargo theft, mishandling. |

| Geographic Boundary | Between countries. | Within a single country's borders. |

| Example Shipment | A case of watches from Geneva to NYC. | Moving inventory from your store to a trade show. |

This table makes it clear: these two coverages are partners, not competitors. One picks up right where the other leaves off, ensuring your assets are protected every step of the way.

Marine and cargo insurance has become a cornerstone of global trade. According to the International Union of Marine Insurance (IUMI), total global marine insurance premiums hit roughly USD 39.92 billion. Cargo insurance alone made up USD 22.64 billion of that, or about 56–57% of the entire market.

For jewelers, that scale is important. Your high-value pieces move through the same global logistics infrastructure as other major commodities, meaning they're exposed to the same systemic risks. A disruption at a major port or a new piracy threat affects everyone.

Decoding Your Policy: What Is Actually Covered?

Trying to read an insurance policy can feel like you’re learning a new language. But for a jeweler, getting the hang of the fine print isn’t just a good idea—it’s the one thing that separates a devastating loss from a manageable hiccup. The entire foundation of your marine and cargo insurance rests on one critical choice: the type of policy you have.

There are two main flavors out there: ‘Named Perils’ and ‘All-Risk’. They might sound similar, but in reality, they’re worlds apart in the protection they offer. A Named Perils policy is basically a strict checklist. It only covers the exact risks spelled out in the policy, like a fire or a truck collision. If your loss happens for any other reason? You’re not covered.

An All-Risk policy, on the other hand, flips that on its head. It covers everything unless a risk is specifically listed as an exclusion. This creates a much wider safety net, which is precisely why it’s the gold standard for high-value industries like jewelry. The burden of proof shifts to the insurer to prove an exclusion applies, not the other way around.

Why All-Risk Is a Non-Negotiable for Jewelers

In the jewelry business, weird, one-off, and totally unexpected losses can happen. An All-Risk policy is built for the unexpected. This is especially true when it's part of a comprehensive Jewelers Block insurance plan from a specialist agency like First Class Insurance.

This superior structure is designed to cover the very things that keep jewelers up at night:

- Theft and Robbery: Covers everything from a sophisticated heist on a cargo truck to a simple grab-and-run at a sorting facility.

- Transit Accidents: Protects your pieces if they’re damaged in a vehicle crash, a ship collision, or an airplane incident.

- Improper Handling: Provides coverage when a carrier drops, crushes, or otherwise mishandles your package.

- Fire and Water Damage: Protects against disasters that can strike in warehouses or on transport vehicles.

But the real game-changer for jewelers under an All-Risk policy is coverage for mysterious disappearance. This covers that nightmare scenario where a sealed, untampered package arrives, but the jewelry inside is just… gone. Standard policies almost never touch this, leaving you completely on your own.

A Real-World Scenario: Mysterious Disappearance

Let’s play this out. You ship a custom-designed diamond bracelet worth $50,000 to a client. You use a top-tier carrier, pack it like a fortress, and track its every move. The package arrives on time, and the box looks perfect—no signs of tampering at all.

Then your client opens it. The bracelet is gone.

There’s no evidence of a break-in or robbery. It simply vanished into thin air. With a standard Named Perils policy, you’d be out of luck because "mysterious disappearance" isn't a listed risk.

This is where an All-Risk policy, especially within a Jewelers Block framework, proves its weight in gold. Since this type of loss isn't specifically excluded, the policy is designed to kick in. Your agent at First Class Insurance would help you file a claim to recover the bracelet's full value, turning a potential business-ending catastrophe into a documented insurance event. Getting a quote for Jewelers Block that includes this coverage is one of the smartest moves you can make.

Understanding Common Exclusions

Even the best All-Risk policy has its limits. These exclusions aren't there to trick you; they’re meant to carve out risks that are either uninsurable or need their own specialized policies. Knowing what isn't covered is just as important as knowing what is.

Some common exclusions you’ll see in marine and cargo policies include:

- Inadequate Packaging: If an item is damaged because it wasn't packed well enough for the journey, a claim can be denied.

- War and Political Risks: Losses from war, strikes, riots, or civil unrest are usually excluded, but you can often add this coverage back with a special endorsement.

- Inherent Vice: This is a term for a natural flaw in the goods themselves that causes damage without any outside help (think of fruit spoiling in transit).

- Deliberate Misconduct: Insurance will never cover intentional damage or illegal acts committed by the policyholder.

By understanding these terms, you can have a smarter conversation with your insurance professional. Together, you can spot potential gaps and add endorsements to build a policy that truly fits your business.

Valuation Clauses for High-Value Jewelry

In the world of high-value jewelry, the gap between an appraised value and what an insurance policy actually pays out can be terrifyingly wide. This is exactly where valuation clauses come in. They are the absolute heart of your marine and cargo insurance policy, defining precisely how your assets will be valued if a loss occurs.

For a jewelry business, getting this right isn’t just a detail; it’s everything. The value of a custom-designed piece isn’t just its raw materials—it’s the artistry, the hours of skilled labor, and the market demand. A strong policy from a specialist like First Class Insurance Jewelers Block Agency gets this from the get-go.

Agreed Value: The Gold Standard for Jewelry

When it comes to insuring jewelry, you'll mainly see two valuation methods: Actual Cash Value (ACV) and Agreed Value. ACV policies pay you the replacement cost of an item minus depreciation. That might work for a company car or a computer, but it’s a disastrous model for jewelry, where unique pieces often appreciate and their value is tied to craftsmanship, not age.

That's why Agreed Value is the only way to go for jewelers.

With an Agreed Value policy, you and the insurance company agree on the exact worth of your items before the ink is even dry on the policy. If a covered loss happens, the insurer pays that full, pre-determined amount. No arguments, no deductions for depreciation. It provides total certainty and is essential for protecting one-of-a-kind or irreplaceable pieces.

Imagine you're shipping a vintage emerald necklace valued at $80,000. Under a typical ACV policy, an adjuster might try to argue depreciation or offer a lower "cash value," leaving you short. With an Agreed Value policy, that $80,000 value is already locked in. You’re made whole for its true market value, period.

The Sue and Labor Clause: Saving a Shipment from Disaster

Beyond valuation, your policy contains clauses that empower you to take action in a crisis. One of the most important is the Sue and Labor clause. Think of it as your policy’s emergency response fund.

If a shipment is in immediate danger—maybe a truck breaks down in a sketchy area, or a crate gets damaged at the port—this clause requires you to take reasonable steps to protect the property from getting worse. But here's the best part: it also covers the reasonable expenses you rack up while doing so.

Need to hire emergency security on the spot? Have to arrange for an armored car to move the goods to a secure vault? Those costs are covered. This proactive clause prevents a small problem from snowballing into a total loss, which is good for both you and your insurer. Protecting your assets, like a high-value diamond engagement ring, is a shared responsibility, and this clause is proof of that partnership.

{kind=link}

Essential Endorsements for Every Jeweler

A standard marine and cargo policy is a great foundation, but a jewelry business operates in a unique world that demands special add-ons, known as endorsements. These are what tailor your coverage to fit the specific risks you face every day.

Here are a few vital endorsements every jeweler should have on their radar:

- Exhibition and Trade Show Coverage: This extends your protection to inventory while it's on display at trade shows—a notoriously high-risk environment far from the safety of your vault.

- Traveling Salesperson Coverage: This protects jewelry while it is in the care, custody, and control of your sales reps out on the road.

- Goods on Consignment/Memorandum: This ensures that pieces you’ve sent to other retailers or have taken in from designers are covered, whether they're in transit or at another store.

By working with an expert to add the right endorsements, you transform a generic policy into a precision shield built specifically for the way your business runs.

Best Practices for Managing Transit Risk

While marine and cargo insurance is your ultimate safety net, the best claim is the one you never have to file. Think of proactive risk management as your first and most effective line of defense. By building strong protocols into your shipping process, you’re not just protecting your inventory—you’re showing underwriters that you’re a low-risk client, which can directly translate into better policy terms and lower premiums.

This isn't about adding busywork to your day. It’s about making smart, strategic decisions that protect your assets, your reputation, and your bottom line.

Fortify Your Shipping Protocols

The single most important decision you can make is choosing the right shipping partner. For a jeweler, trusting high-value pieces to standard carriers like FedEx or UPS is a massive gamble. Their liability is almost always severely limited, and their entire system simply isn't built for the security needs of our industry.

You need to partner with specialists.

- Use Armored Couriers: Companies like Brinks and Malca-Amit are the gold standard for a reason. They provide secure, armed, and fully insured transit designed specifically for high-value goods like jewelry.

- Implement Dual-Control Procedures: A single person should never, ever pack a valuable shipment alone. Always have a second person present to verify the contents and witness the package being sealed. This simple step creates a crucial check-and-balance system.

Following these steps builds a chain of custody that is far more difficult for thieves to breach. More importantly, it gives you concrete proof of your diligence if you ever do need to file a claim.

Discretion and Documentation Are Key

Criminals are opportunists, and a package that screams "valuable contents" is a magnet for theft. Your entire packing and documentation process needs to be built around subtlety and meticulous records.

One of the cardinal rules of shipping jewelry is to use nondescript packaging. The box should give no clue as to what's inside. Avoid using your company's name or any branding that could identify it as a jewelry store.

On top of that, rock-solid documentation is your best friend during a claims investigation. Get in the habit of video-recording the entire packing process. The footage should clearly show the item being placed in the box and the final seal being applied. Keep detailed shipping logs with tracking numbers, courier information, and delivery confirmations. For high-value items, utilizing tamper evident bags is another essential layer, providing immediate visual proof if a package has been opened in transit.

The urgency for these protocols is only growing. Recent data shows cargo theft incidents jumped by a staggering 27% in just one year, with the average loss soaring to over $202,000 per event. Organized criminal groups are actively targeting high-value, portable goods, and that's forcing underwriters to tighten their terms. A jeweler with documented, secure procedures and vetted couriers will always be in a stronger position to secure the best possible marine and cargo insurance.

Navigating the Claims Process After a Loss

Even with the best planning, the world of global shipping has a way of throwing curveballs. Losses happen. When they do, a calm, methodical approach is your best friend. The claims process doesn't have to be a nightmare, especially when you know the steps and have the right advocate in your corner.

The first few moments after you discover a loss are the most critical. Acting quickly and decisively sets the stage for a smooth resolution and ensures your insurance for a jewelry store works exactly as it should.

Your Immediate Action Plan

As soon as you suspect or confirm a loss, the clock starts ticking. Any delay can complicate the investigation and even put your claim at risk. Your first moves need to be automatic.

Here’s exactly what to do right away:

- Notify the Carrier: Put the shipping company on notice immediately—and do it in writing. This is a non-negotiable first step for almost any claim.

- Contact Your Agent: Your next call is to your insurance agent. A specialist at First Class Insurance will walk you through the insurer's specific requirements and start fighting for you from day one.

- File a Police Report: If there's any chance of theft, a police report is essential. This official document serves as a formal record and critical evidence for your claim.

The Critical Role of Documentation

Once you’ve made the initial calls, your focus has to shift to documentation. A strong claim is built on a foundation of solid, undeniable proof. The adjuster assigned to your case needs to piece together what happened, and your paperwork is how they do it.

A well-documented shipment is a defensible claim. The more detailed your records, the fewer questions an adjuster will have, which drastically speeds up the resolution process.

Being able to produce these documents cleanly and quickly is vital. Get ready to provide:

- Proof of Shipment: Your bill of lading or air waybill.

- Proof of Value: The commercial invoices and packing slips that establish what the items are worth.

- Proof of Loss: A formal survey report or clear photos showing the damage.

- All Correspondence: Keep a detailed record of every conversation and email with the shipping carrier.

A specialist agent from a top-tier Jewelers Block insurance agency makes the entire process manageable. They cut through the jargon, handle the communications, and make sure your claim is presented in the strongest possible light, helping your business get back on its feet without missing a beat.

Your Marine Insurance Questions Answered

When you’re dealing with high-value assets constantly on the move, the details of your insurance policy matter. Getting your head around the specifics of marine and cargo coverage can feel like a lot, but a few key distinctions can make all the difference.

Let's break down some of the most common questions jewelers have.

Is Marine And Cargo Insurance Included In My Jewelers Block Policy?

Not always, and that’s a critical detail to confirm. A basic Jewelers Block policy might only cover the inventory sitting inside your four walls, leaving you completely exposed the second a package leaves your hands.

A truly comprehensive policy, however, is built with this risk in mind. It should have transit coverage woven directly into its DNA, protecting you against both inland and ocean marine risks. You need to dig into your policy’s "Goods in Transit" sub-limits and make sure they’re high enough to cover your typical shipments. When you get a quote for Jewelers Block, make sure it explicitly spells out this protection.

Is The Insurance Offered By My Shipping Carrier Enough?

Absolutely not. Relying on the standard insurance from your shipping carrier is one of the biggest gambles a jeweler can take.

Think about it: their liability is almost always capped at a laughably low amount, sometimes just $50 or $100 per package. That’s pocket change compared to the value of a single piece of fine jewelry. What's more, their "coverage" is rarely true insurance; it's often a limited liability agreement riddled with exclusions that can leave you with nothing.

To be made whole for the full, agreed-upon value of your goods—especially against risks like mysterious disappearance—you need a dedicated policy from a specialist in insurance for jewelry business.

What Is The Difference Between FOB and CIF Shipping Terms?

These are more than just acronyms on a shipping document; they determine who’s on the hook for insuring your goods and when. Getting this right is fundamental to managing your insurance for a jewelry store.

- FOB (Free on Board): With FOB, responsibility shifts to you—the buyer—once the goods are loaded. This means you must arrange your own marine insurance for the main leg of the journey.

- CIF (Cost, Insurance, and Freight): Under CIF, the seller is the one responsible for arranging and paying for the insurance.

For any jeweler importing valuable merchandise, you almost always want to operate under a FOB arrangement. It puts you in the driver’s seat, allowing you to work with your own Jewelers Block provider to guarantee you have the broad, ‘All-Risk’ coverage you know and trust. Leaving it in the hands of an overseas supplier is a risk you don't need to take.

The global marine cargo insurance market is only getting bigger, projected to hit around USD 50 billion by 2032. For jewelers, this growth means more sophisticated and integrated insurance options that can seamlessly connect every step of your supply chain under one policy. You can discover more insights about this expanding market and what it means for the industry.

Protecting your inventory from every angle requires a partner who lives and breathes the unique risks of the jewelry trade. At First Class Insurance, we specialize in building Jewelers Block insurance policies that provide comprehensive marine and cargo insurance designed for your specific operation. Don't leave your most valuable assets unprotected during transit—get a quote today and ship with confidence.